Revisiting SPACs in 2026

Revisiting SPACs in 2026

SPACs are back in terms of volume…

A few years ago I wrote a couple of posts that touched on the subject of Special Purpose Acquisition Companies:

Astra Space Given Delisting Warning

Rainwater Tech Joins the SPAC Crowd

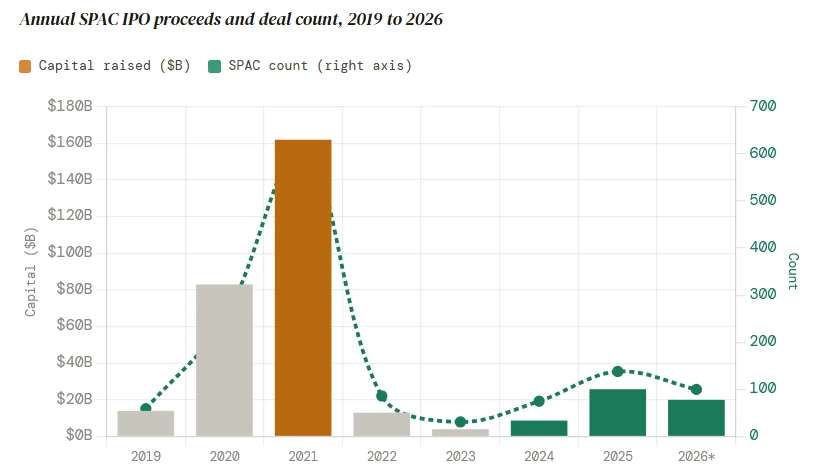

Needless to say, I was apprehensive at best regarding these structures and perhaps veering toward a more outright cynical approach based on some of the transactions we had seen. After 613 SPACs raised $162 billion in a single (and very farcical) year, the fallout led to revamps of capital markets law, sponsor economics, and the very meaning of a credible public listing. Here is a general account of what broke, what’s been altered, and where this type of blank check funding stands heading into mid-2026.

The SPAC cycle of 2020 to 2022 was one of the most compressed boom/bust episodes in modern securities history. Shell companies with no operations, zero revenue, and very often no identified acquisition targets raised hundreds of billions from a slew of investors operating within a range of realms. The resulting legal and structural wreckage was considerable. The lessons learned are now encoded in SEC rules, Delaware court doctrine, and a fundamentally redesigned version of the product itself. The entity that has recently returned is nearly unrecognizable compared to what drew celebrities, athletes, and first-time sponsors into the market just a few years ago.

Four Eras

SPACs are not new. The structure dates to the early 1990s, but has evolved through four recognizably distinct phases, each shaped by different regulatory environments, investor bases, and incentive structures.

1990s – 2009

SPAC 1.0: Wide open

Minimal oversight. Fraud rates exceeded 25%. Deal sizes of $20M to $50M. Penny stock promoters dominated. No institutional participation.

2010 – 2019

SPAC 2.0: Institutional Legitimacy

Trust accounts and redemption rights arrived. Only 15 to 25% of deals created lasting shareholder value. Misaligned incentives persisted.

2020 – 2022

SPAC 3.0: The Bubble

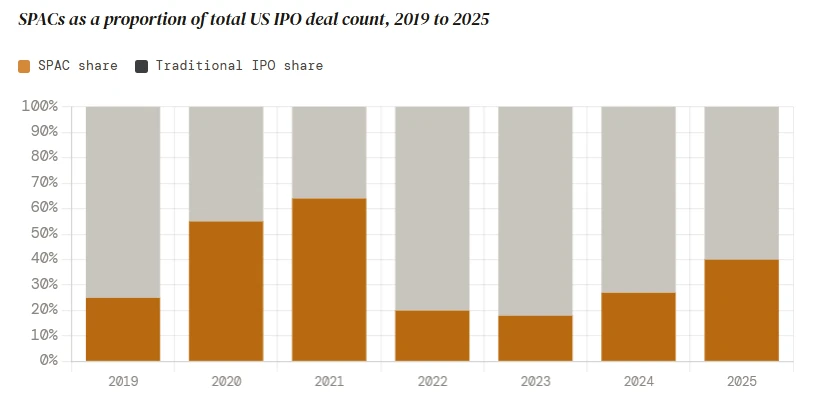

Celebrity sponsors. Retail inanity. SPACs accounted for 64% of all US IPOs at peak. Pre-revenue targets valued at billions then catastrophic collapse.

2024 – Present

SPAC 4.0: Disciplined Return?

SEC rules. Performance-based sponsor economics. Co-registrant liability for targets. Institutional sponsors only. PIPE capital as the structural backbone.

The SPAC 3.0 phase is the one requiring the most attention. At the 2021 peak, 613 SPACs raised $162 billion in a single year. The post-merger performance was one of wreckage as over 90% of De-SPAC companies eventually traded below their $10 IPO price. High-profile failures including Nikola, Lucid Motors, and WeWork shared a common and fairly predictable thread of weak due diligence, speculative forward projections presented without meaningful legal accountability, and structural incentives that rewarded sponsors regardless of whether investors made money. The latter was always a laughably inane component.

The Numbers

The scale of the boom and the depth of the contraction are interesting to examine by viewing some of the basic numbers. SPAC IPO volume collapsed from its 2021 peak by more than 90% before beginning a structurally more sound recovery in 2024 and 2025.

• 613 SPACs launched at 2021 peak

• $162B capital raised in 2021 alone

• 90%+ De-SPACs trading below $10 post-merger

• $25.8B Capital raised in the 2025 recovery

• 40% Of US IPO deal count in 2025

• 184 SPACs filed to list by late 2025

Three Structural Flaws That Caused the Collapse

Attributing the bust to simple market excess misses deeper structural causes.

• Sponsor promotion

The founding architecture of SPAC in its third stage gave sponsors approximately 20% of post-IPO equity at nominal or no cost in exchange for organizing the vehicle and finding a target. This arrangement created powerful incentives to complete any deal within the two year window, regardless of valuation quality. Sponsors faced essentially no financial downside from a bad merger while public shareholders faced holding the proverbial bag.

The dilution arithmetic was beyond inane. A SPAC that raised $500 million might issue 10 million founder shares to its sponsor for a few million dollars. After the merger, if investors exercised redemption rights and the sponsor still closed the deal using PIPE (Private Investment in Public Equity) financing, the remaining public shareholders held a far smaller fraction of the combined company than anticipated. Dilution from warrants issued alongside IPO units compounded the problem further.

• Forward projections exemption/immunity/protection

One key selling point of the SPAC structure to acquisition targets was that forward looking financial projections could be included in de-SPAC registration statements with the benefit of the Private Securities Litigation Reform Act’s safe harbor. Traditional IPOs do not enjoy this protection in the same manner, and the practical result was that SPAC targets could make multi-year revenue and EBITDA projections with relative impunity. Speculative estimates appeared in registration statements as though comparable to audited financials. The SEC’s 2024 rulemaking explicitly aligned the treatment of projections in de-SPAC transactions with those applicable to traditional IPOs thus removing much of the perceived shelter.

• Undisclosed conflicts of interest

Delaware courts identified a related problem in the post collapse litigation wave that ensued. Multiple cases established that SPAC directors owe fiduciary duties to public shareholders, not just to sponsors. Courts found that sponsors’ financial stake in completing any transaction, combined with their control over the vote, created material conflicts of interest that had not been adequately disclosed to investors at the moment they needed to decide whether to redeem their shares.

What the 2024 SEC Rules Actually Changed

The SEC spent nearly two years developing its SPAC rulemaking, proposing regulations in March 2022, and adopting final items on January 24, 2024 with an effective date of July 1, 2024. The final outlines were unsurprisingly narrower than originally proposed in many respects, but still represented a fairly significant overhaul of the SPAC regulatory framework since the structure’s modern inception.

|

Requirement |

What changed |

Primary impact |

Status |

|---|---|---|---|

|

Sponsor disclosure |

Detailed revelation of sponsor compensation, founder share amounts, warrant dilution, and all actual or potential conflicts of interest |

SPAC sponsors and affiliates |

In force July 2024 |

|

Projection alignment |

Forward-looking statements in de-SPAC filings now treated equivalently to traditional IPO projections. Broad safe harbor removed |

All de-SPAC registrants |

In force July 2024 |

|

20-day dissemination period |

Proxy statements for business combination votes must be delivered to shareholders at least 20 days before the meeting date |

SPAC public shareholders |

In force July 2024 |

|

iXBRL tagging |

Enhanced disclosures under new Regulation S-K Item 1600 must be tagged in Inline XBRL format for machine-readable investor comparison |

SPAC and de-SPAC filers |

Required June 2025 |

|

Underwriter liability expansion |

Proposed rule would have extended Section 11 liability to de-SPAC underwriters. Ultimately dropped from the final rules after industry pushback |

Investment banks |

Proposed only |

|

Co-registrant requirement |

Target company must co-sign the de-SPAC registration statement and assume Securities Act Section 11 liability for its accuracy |

Target companies and their directors and officers |

In force July 2024 |

The most consequential change for practitioners is the co-registrant requirement. Before 2024, target companies in de-SPAC transactions did not formally assume legal responsibility for the accuracy of the SPAC’s registration statement. This meant that disclosure quality was only as good as the sponsor chose to make it. What could possibly go wrong under this structure… In the new framework, the target’s directors and officers sign onto the registration statement and face Section 11 exposure identical to a traditional IPO. In practice, this has made de-SPAC transactions look increasingly like traditional offerings in terms of rigor and documentation standards.

The inevitable litigation

While the SEC built its regulatory response, securities class action legal proceedings ran in parallel. The post-2021 collapse produced a wave of lawsuits centered on two main areas: conflicts of interest not disclosed at the time of the merger vote, and misrepresentations about target companies’ business prospects. Several high-profile suits survived motions to dismiss, and at least one was resolved through a settlement exceeding $100 million.

Ongoing litigation risk persists even under the new regulatory framework. The enhanced disclosure requirements actually create a new structure whereby a statement that is disclosed but turns out to be inaccurate or misleading is, if anything, more legally exposed than one that was simply absent. Practitioners in 2026 are closely watching how courts interpret the new co-registrant liability framework in the first generation of cases arising from post-July 2024 de-SPAC transactions.

SPACs rebuilt

The 2025 recovery and the pipeline building into 2026 reflect a market that has internalized, at least to some degree, the lessons of the collapse. The structural characteristics of current SPAC transactions differ thusly:

|

Structural feature |

2020 to 2022 |

2024 to present |

|---|---|---|

|

Sponsor economics |

20% promote, minimal capital at risk, vested on deal close regardless of stock performance |

Performance-based vesting, earnouts tied to share price thresholds, greater sponsor capital at risk upfront |

|

Deal timelines |

Compressed, often under 12 months, to beat the two-year deadline; due diligence rushed accordingly |

Longer timelines with rigorous diligence, target co-registrant legal review adds preparation burden |

|

Target quality |

Pre-revenue, concept-stage companies accepted; speculative multi-year projections routine |

Emphasis on revenue-generating targets with auditable financials and realistic valuation expectations |

|

PIPE financing role |

Secondary; often absent or thin, particularly in scenarios with high public redemptions |

Essential; committed PIPE capital is now the primary mechanism for closing deals despite high redemption rates |

|

Sponsor profile |

First-time promoters, celebrities, sector generalists with limited operating track records |

Experienced, repeat sponsors with credible sector focus, institutional relationships, and reputational capital at stake |

|

Disclosure standard |

Below traditional IPO standard; forward projections shielded by broad PSLRA safe harbor |

Equivalent to traditional IPO; target co-signs registration statement; PSLRA treatment fully aligned |

The PIPE market deserves particular attention. In the SPAC 3.0 era, high redemption rates (often 80 to 95% of public shareholders electing to take their $10 back rather than hold through the merger) were treated as structural failure signals. In 2026, high redemptions are accepted as a feature of the landscape rather than a crisis. The critical question is whether committed PIPE capital can cover the shortfall. Several deals in 2025 closed successfully despite redemption rates in the nineties because PIPE commitments were fully secured before the shareholder vote. This transforms the role of institutional investors as they are effectively the underwriters of the transaction in all but formal name.

Digital asset anomaly

One unusual chapter in the 2025 SPAC recovery was the rise of the digital asset treasury strategy. Multiple de-SPAC transactions in early 2025 involved contributing large crypto holdings into the combined company as the primary business rationale. The approach drew enormous attention, reflecting both the broader crypto market rally and a recognition that SPACs remained one of the fastest paths to listing an adjacent business.

That momentum cooled by the middle of that year as crypto volatility, combined with rapid market saturation as too many similar vehicles chased institutional capital simultaneously, deflated the strategy. The episode illustrates a structural reality of the SPAC product in that its speed and flexibility make it attractive in hot, often overblown markets, and that same speed makes it vulnerable to exhaustion faster than traditional IPO pipelines can adjust.

Where things currently stand

As of the first half of 2026, the signals are cautiously constructive. Fifty SPACs raised a combined $10 billion in the first two months of the year alone, compared to 24 traditional IPOs collecting $7 billion over the same period. The pipeline of filed SPACs stood at 184 as of late 2025, a number more than double the 75 that filed across all of 2024. Experienced, repeat sponsors are leading this wave with seemingly conservative structures and a bit of demonstrated sector credibility.

The risks that could derail the recovery are also visible. The number of vehicles competing for a finite pool of attractive private targets creates, as usual, deal quality pressure. Sponsors unable to find credible targets within the search window face the same liquidation dynamic that torched the 2022 to 2023 period. The new SEC disclosure requirements, while broadly welcomed as a legitimizing force, extend deal timelines and raise preparation costs in ways that disadvantage smaller or less resourced sponsor teams.

The Nasdaq delisting rule change proposed in July 2024, which addresses the suspension and delisting of SPACs failing to complete combinations within required timeframes, adds a layer of regulatory accountability that did not exist during the boom years. Together, these structural guards represent the most tangible institutional memory of what went wrong.

Lessons…?

The SPAC cycle of 2020 to 2022 produced a substantial body of legal doctrine, regulatory rulemaking, and structural redesign. The lessons that appear to have perhaps taken hold are those that aligned incentives rather than just increasing disclosure volume. Performance based sponsor economics matter more than additional checkboxes. The co-registrant requirement is important because it places real legal exposure precisely where information asymmetry previously was found. The PIPE market’s new centrality carries more weight because it replaces retail speculation with informed institutional capital as the actual source of deal financing.

What has not changed is the underlying tension in the SPAC structure that has speed and flexibility on one side, and the rigor that long-term investor protection requires on the other. The new framework manages this tension better than its predecessors, but whether it manages it well enough will be answered not in the filings pipeline but in the post-merger performance of the companies going public through this route over the next three to five years.