The State of Programmatic Advertising in 2026

The State of Programmatic Advertising in 2026

How automated media buying has matured, where the friction points remain, and what’s coming next.

The broad basics are familiar: advertisers use technology platforms to bid in real time for ad placements across a sprawling inventory of websites, apps, connected television, and digital audio. What has changed considerably is the sophistication of the underlying mechanisms, the regulatory environment in which it operates, and the degree to which artificial intelligence has become a primary driver of outcomes.

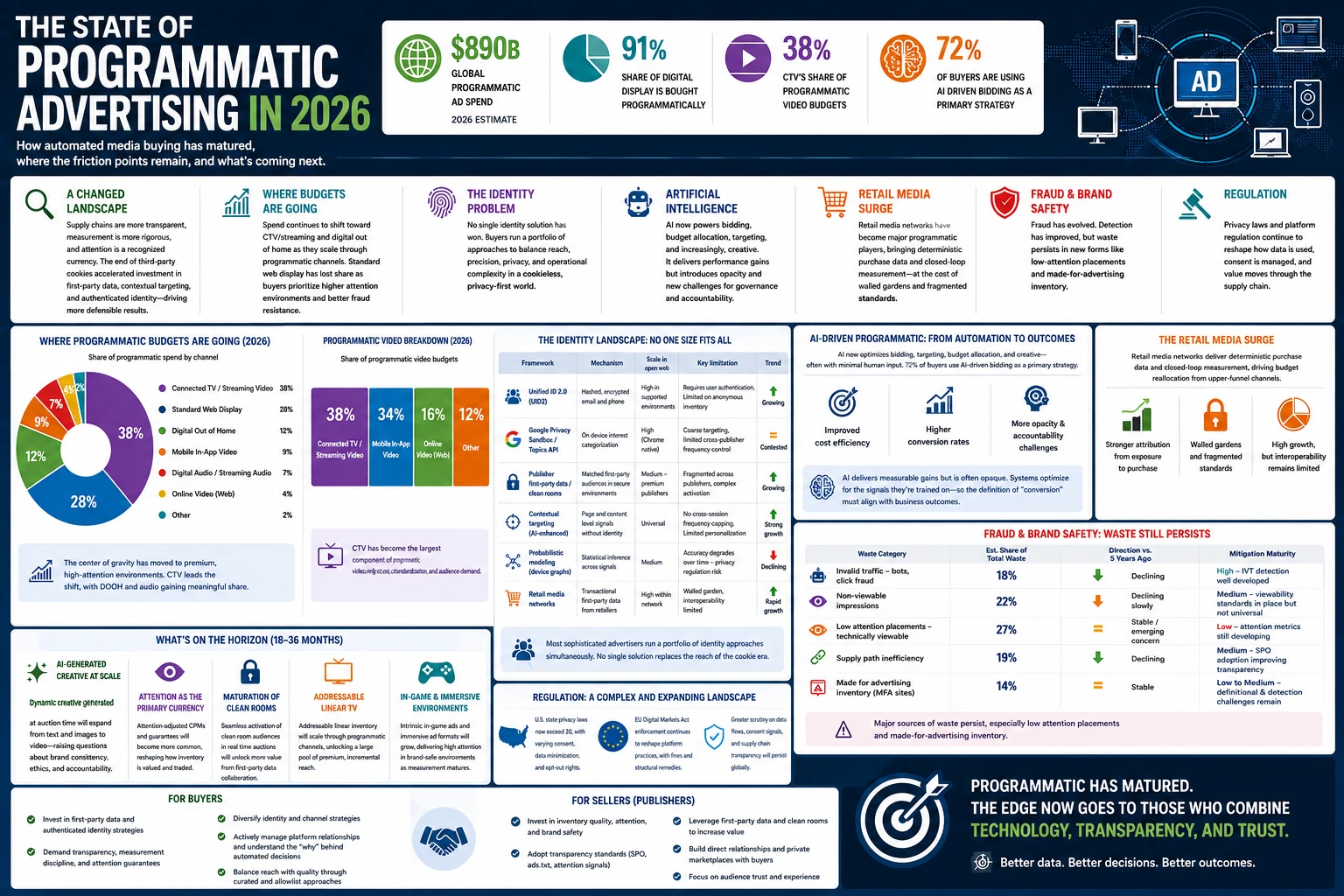

• $890 billion global programmatic ad spend – 2026 estimate

• 91% share of digital display is bought programmatically

• 38% CTV’s share of programmatic video budgets

• 72% of buyers are using AI driven bidding as a primary strategy

A Changed Landscape

The version of programmatic advertising that existed less than 10 years ago was already technically impressive but operationally chaotic to say the least. The supply chain was notoriously opaque, with ad dollars passing through so many intermediary hands that independent audits routinely found that less than half of a campaign’s budget reached a working impression. Measurement was a mess, viewability was widely gamed, and the promise of precise audience targeting was routinely undermined by stale data and mismatched identity graphs.

A good deal of that has improved as the IAB’s Supply Chain Object standard, along with broader adoption of more proper verification methods, has made it meaningfully harder to route budget through fraudulent intermediaries. Measurement providers have consolidated around more rigorous methodologies, and the rise of attention metrics as a trading currency alongside traditional click and viewability signals has given buyers a more honest picture of what they are actually purchasing.

At the same time, the closure of the third-party cookie in Chrome, which finally occurred in full force through 2024 and 2025, reshaped audience targeting in ways the industry spent years bracing for but still found disruptive. The transition accelerated investment in first party data infrastructure, contextual targeting, and identity resolution frameworks built around authenticated users rather than tracked browsers. None of these solutions is as frictionless as the old model was, but a growing number of sophisticated buyers would argue they are producing more defensible results.

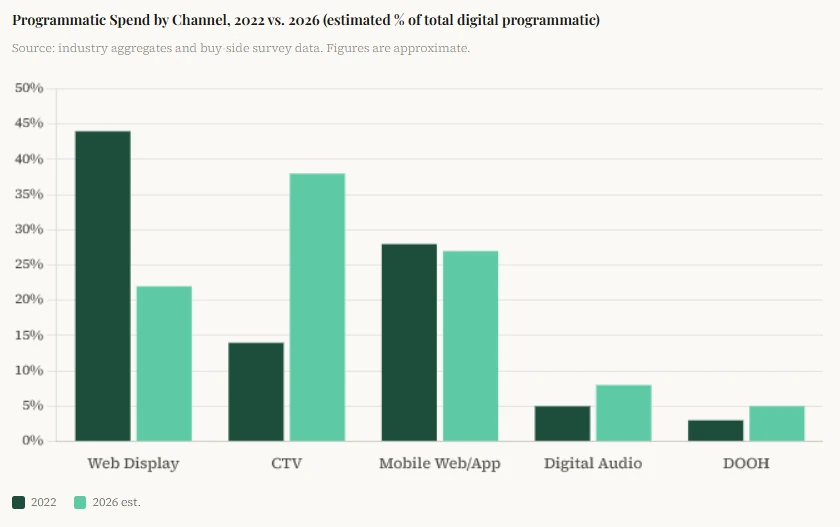

Where budgets are going

The most consequential shift in programmatic spend over the past few years has been the continued migration toward connected television and streaming audio. These environments were once considered premium but cumbersome, lacking the scale and standardization of web display. That gap has closed considerably as CTV inventory now flows through the same DSPs that buyers use for display and video, and the major streaming platforms have opened things enough to participate in programmatic auctions, albeit with varying degrees of openness and transparency.

Digital out of home service has also grown into a legitimate programmatic channel. The infrastructure build out of the prior decade produced a vast network of screens in transit hubs, retail environments, and urban areas that can now be activated dynamically based on audience, weather, time of day, or inventory triggers. It remains a small portion of total programmatic budgets at this point, but the upward trajectory is fairly clear.

Standard web display, by contrast, has continued to lose share. This does not mean it has become irrelevant as retargeting and prospecting campaigns in this realm continue to deliver acceptable performance for certain categories. However, the era of this approach as a primary prospecting channel is largely over for most advertisers, replaced by environments where attention is higher and fraud is structurally more difficult to execute at scale.

The identity problem

The deprecation of third-party cookies prompted the industry to develop a range of identity solutions, none of which has emerged as a clear universal standard.

|

Framework |

Mechanism |

Scale in open web |

Key limitation |

Trend |

|---|---|---|---|---|

|

Unified ID 2.0 (UID2) |

Hashed, encrypted email and phone |

High in supported environments |

Requires user authentication. Limited on anonymous inventory |

Growing |

|

Google Privacy Sandbox / Topics API |

On device interest categorization |

High (Chrome native) |

Coarse targeting, limited cross-publisher frequency control |

Contested |

|

Publisher first-party data / clean rooms |

Matched first-party audiences in secure environments |

Medium – premium publishers |

Fragmented across publishers, complex activation |

Growing |

|

Contextual targeting (AI-enhanced) |

Page and content level signals without identity |

Universal |

No cross-session frequency capping. Limited personalization |

Strong growth |

|

Probabilistic modeling (device graphs) |

Statistical inference across signals |

Medium |

Accuracy degrades over time – privacy regulation risk |

Declining |

|

Retail media networks |

Transactional first-party data from retailers |

High within network |

Walled garden, interoperability limited |

Rapid growth |

In practice, most sophisticated advertisers are running a portfolio of identity approaches simultaneously, using different methodologies for varied segments of their media plan and accepting that no single approach will provide the seamless reach of the previous era. This is a reasonable accommodation, even if it adds operational complexity and makes attribution considerably more difficult.

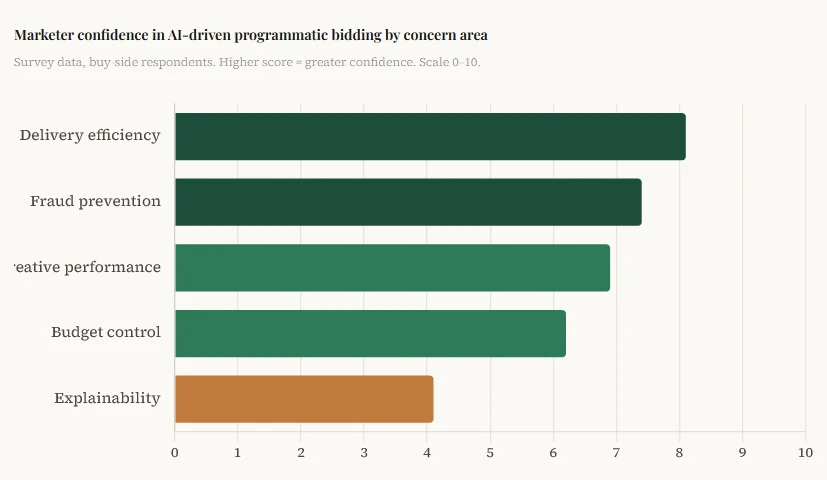

Artificial intelligence

The integration of machine learning into programmatic buying is not new, but the depth of that merging has increased to a point where, for many campaigns, a human buyer’s primary interaction with the system is setting goals and reviewing outcomes rather than managing bids, adjusting targeting parameters, or optimizing creative rotation. This is a material change in the nature of the job, and it carries substantial implications for accountability.

AI driven bidding strategies have in many cases produced measurable improvements in cost efficiency and conversion rates. The results are often impressive in aggregate, but they are also opaque in ways that make it difficult for buyers to understand why a given decision was made or to intervene when something is going wrong.

This gap is one of the more persistent frustrations in the current market. Buyers who would never accept a media plan from an agency without supporting rationale are routinely utilizing campaign architectures from platforms where the decision logic is essentially inaccessible by design. The providers argue, not without some justification, that revealing the logic would make the systems gameable. Critics maintain that buyers cannot manage what they are unable to comprehend. Both points have merit, and the concerns of both sides are unlikely to be resolved soon.

There is also the question of what functionalities AI actually addresses. Systems trained on conversion signals will optimize toward those, which sounds obvious until you examine what events a platform classifies as a conversion and realize that the definition may not align with what the advertiser actually requires.

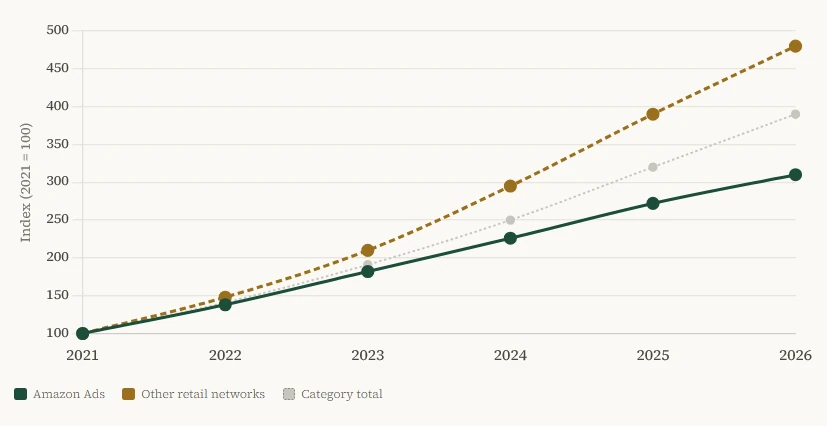

The retail media surge

One development has genuinely surprised the industry in terms of its speed and scale is the rise of retail media networks as major programmatic players. Amazon’s advertising business has been a known force for years, but the proliferation of these alternative networks across grocers, mass merchants, home improvement chains, and specialty merchants has created a new tier of premium programmatic inventory that comes with something most open web stockpiles can’t offer: deterministic purchase data.

The appeal is fairly clear. A consumer goods brand buying ads on a major grocer’s network can directly connect message exposure to in store and online purchase, closing the attribution loop in a way that display or even search advertising cannot match. This has driven significant budget reallocation away from top of the funnel digital channels and toward retail media placements that offer demonstrable, closed loop measurement.

The complications are equally apparent as each retailer runs its own walled garden with targeting capabilities, measurement methodologies, and reporting interfaces specific to their realm. The industry has made some progress toward standardization through the IAB’s Retail Media Standards, but the work is far from complete and individual networks have little economic incentive to make it easier for advertisers to compare their performance directly against competitors.

Fraud and brand safety

Ad fraud has certainly not been eliminated, but it has been more professionalized and, in some respects, made more sophisticated by the same AI capabilities that advertisers are using to optimize campaigns. Invalid traffic detection has improved considerably, and the adoption of supply chain transparency standards has made large scale schemes harder to execute at low cost.

|

Waste category |

Est. share of total waste |

Direction vs. 5 years ago |

Mitigation maturity |

|---|---|---|---|

|

Invalid traffic – bots, click fraud |

18% |

Declining |

High – IVT detection well developed |

|

Non-viewable impressions |

22% |

Declining slowly |

Medium – viewability standards in place but not universal |

|

Low attention placements – technically viewable |

27% |

Stable/emerging concern |

Low – attention metrics still developing |

|

Supply path inefficiency |

19% |

Declining |

Medium – SPO adoption improving transparency |

|

Made for advertising inventory |

14% |

Stable |

Low to medium – definitional and detection challenges remain |

Made for advertising websites represent a particularly stubborn problem. These are engineered specifically to generate programmatic revenue rather than to serve genuine audiences, and they have evolved to pass many standard brand safety and viewability checks while delivering impressions that are effectively worthless from an attention standpoint. Blocklists help but are inevitably reactive. Allowlist approaches, where buyers restrict their budgets to a pre-approved set of publishers, sacrifice reach but produce meaningfully better inventory quality.

Brand safety concerns have similarly grown more complex as inventory has expanded into new formats. CTV and streaming offer relatively clean environments but are not immune from adjacency issues, particularly on ad supported tiers of services that aggregate third party content. The tools for monitoring this realm across CTV lag behind what is available in web display, and the industry is actively working to close that gap.

Regulation

The regulatory environment governing programmatic advertising has become considerably more demanding over the past few years. The US has moved from a landscape of one prominent state level privacy law (California) to a melange of more than twenty state frameworks with varying requirements around consent, data minimization, and opt out rights. The EU’s enforcement of the Digital Markets Act has continued to reshape how major platforms operate their advertising businesses in European markets, and several large fines along with structural remedies have produced distinct changes in how consent is managed and the manner in which data flows between parties in the supply chain.

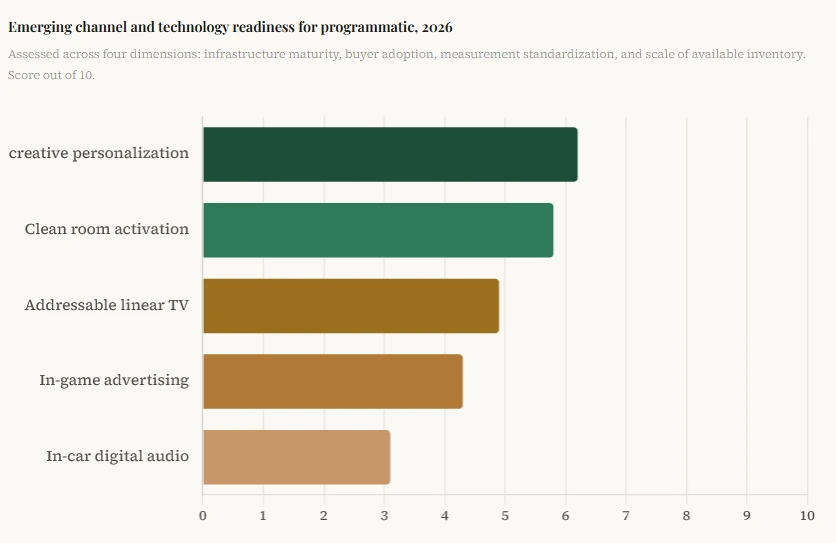

What’s on the horizon

The developments most worth watching in the next 18 to 36 months seem to fall into a few clusters. None of them is a sudden disruption as all are evolutions of trajectories already in motion.

• AI generated creative at scale

The intersection of generative AI and programmatic delivery is beginning to produce campaigns where not just the targeting and bidding but the creative itself is produced dynamically at auction time. Early implementations are primarily in text and static image formats, but video is coming quickly. The implications for creative agencies, brand consistency, and the question of who is legally and ethically responsible for AI produced advertising are significant and will be interesting to watch to say the least.

• Attention as the primary trading currency

A growing number of transactions in premium programmatic markets are being priced on attention adjusted CPM rates rather than raw viewability. These vendors have matured enough to provide third party verification, and a handful of major holding companies have begun to require attention guarantees as part of their programmatic commitments. If this trend continues (and there is reasonable evidence that it should) this will reshape inventory valuation in ways that benefit quality publishers and disadvantage environments that generate impressions without engagement.

• The maturation of clean rooms

These environments where first party data from multiple sources can be analyzed without raw data being shared have become a standard part of the toolkit for sophisticated programmatic operations. What is developing now is the infrastructure to activate clean room audiences directly in auctions without the current blockage of manual data export and upload cycles. If that activation becomes seamless, the value seen as a programmatic targeting input will increase considerably.

• Addressable linear television

The convergence of linear and digital television continues, and addressable TV, meaning linear broadcast inventory sold with individual household targeting rather than demographic guarantees, is moving toward programmatic avenues at a pace that was not possible three years ago. This represents a genuinely large pool of premium inventory entering a programmatic framework for the first time, and it will attract meaningful budget reallocation from buyers who have been waiting for the infrastructure to catch up with the concept.

• In-game and immersive environments

Advertising within video games has been a somewhat slow developing area that has periodically been declared the next major programmatic frontier. The infrastructure is now genuinely more capable than it has been, with intrinsic in game ad formats that place brand imagery within environments without interrupting play, delivered programmatically through DSPs that buyers already use. Scale remains a legitimate constraint, and measurement is in relatively early stages, but the attention quality of gaming audiences has attracted serious interest from categories including automotive, financial services, and consumer electronics.

Considerations for buyers and sellers

Navigating this environment productively requires a realistic view of what programmatic buying can and cannot do. The technology has become genuinely impressive, and the attendant supply chain has grown more trustworthy. The measurement capabilities, while certainly still imperfect, have improved to a point where outcomes based buying is possible across a wider range of formats than it was just a short period ago. At the same time, automation has created distance between buyers and the decisions being made on their behalf, and that requires active management rather than passive trust.

Publishers operating quality environments have more leverage than they have had in years, largely because the industry’s quality problem has pushed serious buyers toward allowlist approaches and private marketplace commitments. The era in which open auction exposure to maximum scale was the dominant strategy is giving way to something more curated and intentional, and that is on the whole a healthier dynamic for the ecosystem even if the transition is uncomfortable for those used to monetizing at volume.

The organizations that will navigate the next phase most effectively are likely those that have invested in first party data infrastructure, that have built genuine measurement discipline into their campaign frameworks, and that approach their platform relationships as something to actively manage rather than simply activate.