2026 First Quarter Venture Funding Results

2026 First Quarter Venture Funding Results

A brief recap of venture capital events during the first quarter of 2026

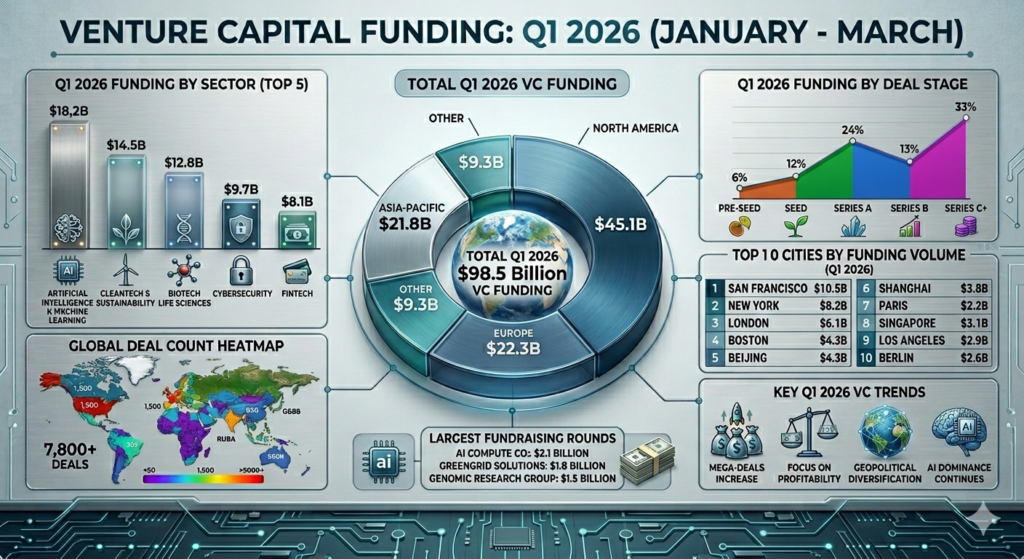

The first quarter of 2026 has officially closed and the data paints a picture of a venture capital landscape that is both maturing and aggressively pivoting toward long-term profitability. After the volatility of the early 2020s, Q1 2026 has emerged as a period of what might be termed disciplined exuberance. Total funding reached $98.5 billion globally across more than 7,800 deals.

A more detailed dive into the trends, sectors, and geographic shifts that defined the start of the year.

The Global Overview: Steady Growth

The first quarter of 2026 didn’t just exceed expectations in venture capital, it reset them entirely. Global startup funding surged to unprecedented levels, driven by massive artificial intelligence AI investments, a handful of historic mega-rounds, and a growing concentration of capital among elite companies.

The total global funding of $98.5 billion represents a healthy 12% increase year-over-year. Investors are no longer sitting on the proverbial sidelines as the accumulated masses of dry powder are finally being deployed, though with much stricter due diligence than in previous cycles. North America remains the dominant force, capturing $45.1 billion of the total monetary allotment while Asia-Pacific and Europe continue to show strength in specialized hubs, particularly in deep tech and sustainability.

Sector Spotlights: AI and Cleantech Lead the Charge

It comes as no surprise that Artificial Intelligence and Machine Learning continue to be the primary engines of VC growth, securing $18.2 billion in Q1 alone. If there is one defining theme of Q1 2026, it is the overwhelming dominance of artificial intelligence. However, the nature of these investments has shifted from general purpose LLMs to a more vertically aligned AI that provides highly specialized applications for healthcare, law, and manufacturing.

Cleantech & Sustainability followed closely with $14.5 billion. As global carbon regulations tighten, we are seeing massive Series B and C rounds for companies focusing on long-duration energy storage and next-generation grid management.

Top Sectors by Funding:

AI & Machine Learning: $18.2B

Cleantech & Sustainability: $14.5B

Biotech & Life Sciences: $12.8B

Cybersecurity: $9.7B

Fintech: $8.1B

The Return of the Mega-Round

Q1 2026 saw the resurgence of the appreciably larger rounds that total $100M+. Large-scale capital infusions were particularly prominent in the AI Compute and Genomic Research spaces. Notable infusions included a $2.1 billion raise by AI Compute Co. and a $1.8 billion outlay for GreenGrid Solutions. Interestingly, while late-stage funding is soaring, Seed and Series A stages are seeing a more tailored approach. Investors are looking for founders who can demonstrate a clear path to profitability within 18 months, rather than focusing solely on user acquisition.

Geographic Hotbeds: Beyond Silicon Valley

While San Francisco ($10.5B) and New York ($8.2B) remain the top two cities for funding volume, the global heatmap shows what might be viewed as a significant decentralization of innovation. London has solidified its place as the top European hub ($6.1B) driven by a surge in fintech to climate pivots. Meanwhile, cities like Singapore and Berlin are seeing record-breaking deal counts in the cybersecurity and logistics sectors.

Key Trends to Watch

As we look toward Q2, three major themes dominate the boardroom:

The Profitability First Mandate: The era of growth at any cost is firmly over. VCs are prioritizing companies with high unit economics and sustainable margins.

Geopolitical Diversification: Funding is increasingly flowing into friendly-shoring tech hubs as companies seek to insulate their supply chains from geopolitical tension.

The IPO Window: With several high-profile AI companies rumored to be filing for IPOs in late 2026, the success of these exits will dictate the appetite for late-stage private funding for the rest of the year.

Risks and Outlook

While Q1’s numbers are impressive, several risks loom:

Overconcentration in AI: Heavy reliance on one sector could create systemic vulnerability.

Mega-round distortion: A few deals are skewing overall metrics.

Geopolitical uncertainty: Trade tensions and regulatory shifts may impact cross-border investment. Nonetheless, investor sentiment remains optimistic. Expectations of major AI IPOs and continued technological breakthroughs are likely to sustain momentum in the near term.