The Anatomy of a High-Tech Executive Offer

The Anatomy of a High-Tech Executive Offer

Modern compensation packages have become elaborate financial instruments. Here’s how equity structures, golden handcuffs, and performance milestones actually work.

When a Fortune 500 board recruits a new Chief Technology Officer, or a late-stage startup courts a seasoned CFO, the conversation rarely centers on salary. The base pay is almost an afterthought as it can readily become a somewhat predictable number buried at the bottom of a very complicated document. What fills the rest of that item is where the real negotiation component lives – a layered construction of equity, incentives, and contingencies designed to align the executive’s interests with the company’s trajectory while simultaneously making it expensive to leave.

Understanding these packages with regard to how they’re structured, what the fine print means, and which elements constitute genuine upside versus gilded constraints has become essential knowledge for anyone operating at the leadership level in tech.

The four pillars of modern executive pay

Most senior tech executive offers are built from four general core components. Their relative proportions shift dramatically depending on company stage, sector, and the individual’s leverage, but the building blocks are nearly universal.

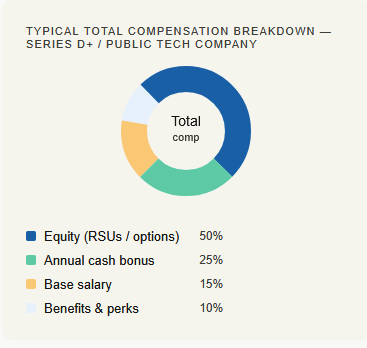

Base salary in tech executive roles is deliberately compressed as a share of total compensation. For example, a Chief Product Officer at a public software company might earn $400,000–$600,000 in salary which may be viewed as competitive in absolute terms, but often this represents less than 20% of their total annual package. This compression is intentional as it signals commitment and aligns executive incentives with shareholder value.

Equity structures: RSUs, options, and the space between

Equity is the centerpiece of virtually every senior tech offer, but the primary instrument used varies significantly. Restricted Stock Units (RSUs) have largely displaced traditional stock options at public companies and late-stage private firms, while options remain common at earlier-stage startups where the current share price is typically low enough to make them meaningful.

RSUs are straightforward in concept. The company promises to deliver a certain number of shares on a future date contingent on continued employment. Their value is easy to model. If the stock price is $50 and you have 20,000 RSUs vesting this year, you can reasonably plan an income of around $1 million. Stock options are more speculative. You receive the right to purchase shares at today’s strike price which only generates profit if the stock climbs meaningfully above that baseline.

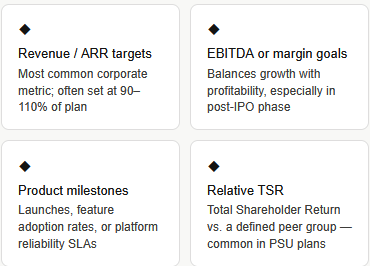

Performance Share Units (PSUs) occupy a middle ground that’s become increasingly common at the C-suite level. These are RSUs with strings attached. The actual number of shares you receive scales up or down depending on whether the company hits predefined targets. A 100% PSU grant might pay out anywhere from 0% to 200% of the target number depending on metrics like revenue growth, EBITDA margin, or relative total shareholder return against a peer group.

The vesting schedule and the cliff

Regardless of the equity instrument, nearly every grant is subject to a vesting schedule which encompasses the calendar year over which you actually earn the shares. The standard in the industry has long been a four-year vest with a one-year cliff.

The cliff means that if you leave (or are let go) before your first anniversary you receive nothing. This is the first of several structural features designed to retain talent. After the cliff, shares typically vest on a monthly or quarterly schedule for the remaining three years.

At the executive level, offer packages routinely include refresh grants that are additional equity units allocated in subsequent years to maintain the executive’s total unvested position and prevent the compensation from becoming backloaded and then rapidly declining. A VP who joined with a four-year grant will, by year three, have only one year left of that original award vesting. Without a refresh, their unvested equity, and therefore their financial reason to stay, has shrunk dramatically.

Golden handcuffs: the architecture of retention

The phrase “golden handcuffs” is informal, but the mechanism is precise. Create financial conditions that make departure genuinely expensive. Unvested equity is the most obvious example, but modern executive packages layer in several additional tools.

Signing bonuses with clawbacks are standard at senior levels. A company might offer a $500,000 sign-on amount but require full repayment if the executive leaves within 18 or 24 months. The practical effect is that the executive needs to generate enough compensation in that window to cover both the clawback and the unvested equity they forfeited at their prior employer.

Non-compete and non-solicit agreements, despite ongoing legal challenges in jurisdictions like California, remain a feature of many executive contracts. Even where unenforceable, they create psychological friction and potential litigation risk, which achieves a similar behavioral effect.

Deferred compensation plans, common at larger companies, allow executives to channel a portion of their bonus or salary into tax-advantaged accounts that only pay out after a vesting or deferral period. The dollars stay on the company’s books meaning they’re also at risk if the organization faces financial distress.

Performance milestones and the variable component

Annual incentive plans commonly called STIPs (Short-Term Incentive Plans) link cash bonuses to a combination of corporate and individual performance metrics. A CRO might have 60% of their bonus tied to company revenue targets and 40% to individual objectives. Miss the corporate number badly enough and even superior personal performance results in a reduced or zero payout.

Long-term incentive plans (LTIPs) extend this logic over three-year periods. The Compensation Committee generally establishes targets at the start of the cycle, and shares (or cash) are awarded at the end based on actual results against those targets. Because the performance period is multi-year, today’s grant won’t resolve until well into the future adding another layer of golden handcuffs for executives who want to participate in the full payout.

Change-of-control provisions: the parachute question

Perhaps the most dramatic element of any senior executive contract is the change-of-control provision that is sometimes referred to colloquially as a “golden parachute.” These clauses activate if the company is acquired or undergoes a significant ownership change.

Double-trigger provisions, now considered best practice by governance advisors, require two events to occur before accelerated vesting kicks in: (1) a change of control, and (2) the executive’s employment being terminated or materially diminished. This prevents a windfall for executives who continue in comfortable roles under new ownership, while protecting those who are displaced. Single-trigger clauses where the acquisition alone accelerates vesting still appear in some contracts but face increasing shareholder opposition.

Severance packages for C-suite executives typically specify cash payments of one to three times base salary plus target bonus, continued benefits for a defined period, and full or partial acceleration of unvested equity. These numbers are negotiated upfront and specified in the contract. By the time they’re needed, the terms have long been set.

What gets negotiated and what doesn’t

Most executives approaching a senior offer negotiation focus their energy on the wrong line items. Base salary adjustments are typically modest as a company will rarely move more than 15–20% from their initial offer at that level. Equity solutions are more flexible, especially in competitive talent markets, though it often requires the candidate to make a compelling case tied to relevant and specific data.

The highest-leverage negotiation points are frequently structural rather than numerical. The length of the vesting cliff, the definition of “good reason” in a termination clause, whether PSU targets are set at grant or annually, and the precise definition of what triggers a change-of-control provision are all of primary consideration here. These terms are often treated as boilerplate but they determine the actual cash value of the package under dozens of scenarios the candidate hasn’t yet imagined.

Experienced executives and their legal counsel also pay close attention to the definition of “cause” for termination. A narrow definition protects the executive; a broad one gives the board significant latitude to terminate without triggering severance obligations. In a volatile tech environment where leadership transitions, strategic pivots, and hostile acquirers are ever-present this language matters enormously.

Equity Incentives Governance

The architecture of executive compensation reflects decades of negotiation between boards, shareholders, and talent which represents a continuous negotiation over how to align interests across different time horizons. For the executive sitting across the table, understanding these structures isn’t just useful context. It’s the difference between accepting a package and actually knowing what you’ve agreed to.