How Satellite Operators Are Reinventing Their Revenue Models Via the Cloud

How Satellite Operators Are Reinventing Their Revenue Models Via the Cloud

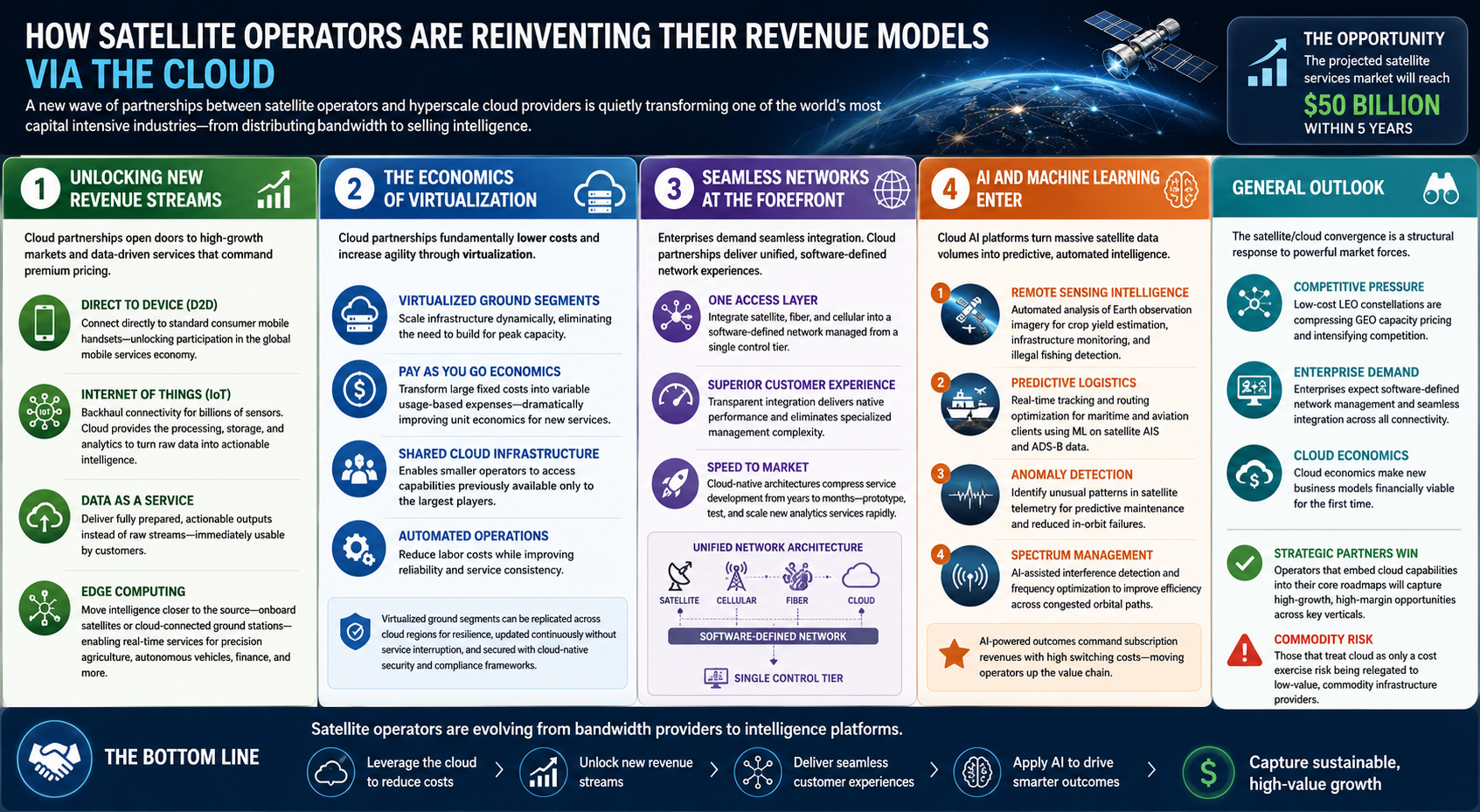

A new wave of partnerships between satellite operators and hyperscale cloud providers is quietly transforming one of the world’s most capital intensive industries from distributing bandwidth to selling intelligence.

For decades, satellite operators occupied a comfortable but fairly narrow lane in the telecommunications economy by owning the machines in orbit, selling capacity to distributors and enterprise clients, and collecting recurring fees for moving data across vast geographies that terrestrial networks could not reach. The business model was relatively stable and, for the largest players, highly profitable.

That model is now being altered in numerous ways. Across the industry, operators from multi-orbit entities to emerging low-earth orbit constellations are building deep strategic partnerships with hyperscale cloud providers in a bid to reinvent themselves as data driven service platforms. The transformation reaches ground infrastructure, business models, customer relationships, and the basic definition of what a satellite company sells.

Understanding why this shift is happening (and why it is occurring now) requires examining what appears to be four primary forces: the search for new revenue streams, the urgent need to cut operational costs, rising customer expectations, and the emergence of artificial intelligence as an applicable business tool. The importance of doing so is clear given that the projected satellite services market will reach $50 billion within 5 years.

1. Unlocking new revenue streams

The most immediate commercial opportunity presented by cloud partnerships is the ability to enter markets that were previously inaccessible. Foremost amongst these is the direct to device (D2D) market which provides the capability to connect directly to standard consumer mobile handsets without any specialized hardware. This effectively represents the potential to participate in the global mobile services economy for the first time.

Equally significant is the integration with the Internet of Things ecosystem. As billions of industrial sensors, agricultural monitors, maritime trackers, and environmental instruments come online, satellite operators are uniquely positioned to provide the backhaul connectivity that terrestrial networks cannot. Cloud partnerships are essential here because they provide the data processing, storage, and analytics infrastructure needed to turn raw sensor data into actionable intelligence and, in doing so, command premium pricing.

Perhaps the most interesting new model is what is being termed data as a service. Rather than simply delivering a stream that a customer must then process internally, operators are now leveraging cloud partnerships to offer fully prepared outputs that are immediately usable.

Edge computing represents yet another viable possibility that we’re seeing via a number of companies we’re working with. By moving intelligence closer to the point of data collection (whether onboard next generation satellites themselves or at cloud connected ground stations) operators can process data in real time and offer services that were previously impossible. This is particularly valuable for applications including precision agriculture, autonomous vehicle coordination, and financial market data.

2. The economics of virtualization

Behind the revenue opportunity is an equally compelling cost story. Traditional satellite operations have been defined by massive amounts of capital expenditure that include not just the cost of building and launching spacecraft, but the elaborate ground segment infrastructure required to operate them. This hardware has historically been proprietary, expensive to maintain, and relatively slow to upgrade.

Cloud partnerships are enabling a fundamental shift in this architecture. Software defined ground stations replace racks of specialized hardware with virtualized functions running on commodity servers and connected to cloud data centers. The result is infrastructure that can be scaled up or down in response to actual traffic demand, upgraded through software rather than physical replacement, and paid for on a consumption basis rather than as an outright capital investment.

• Virtualized ground segments allow operators to scale infrastructure dynamically, eliminating the need to build for peak capacity.

• Pay as you go cloud economics transform large fixed costs into variable usage based expenses which often dramatically improve unit economics for new services.

• Shared cloud infrastructure enables smaller operators to access capabilities previously available only to the largest players in the industry.

• As a result, automated operations lead to reduced labor costs while improving reliability.

The operational benefits of this approach extend beyond simple cost reduction. A virtualized ground segment can be replicated across cloud regions for resilience, updated continuously without service interruption, and audited with the unique observability tooling that cloud platforms provide. For regulated industries like defense and government communications, this also opens the door to cloud based security and compliance frameworks that would typically be impractical to replicate on private infrastructure.

3. Seamless networks at the forefront

Enterprise customers have changed. Where once a satellite link was a specialized tool for remote locations, today’s enterprise network architects expect this to function as a native component of a broader network that integrates transparently with terrestrial fiber, cellular, and cloud services without requiring specialized management or generating an errant user experience.

This now near ubiquitous connectivity mandate is reshaping how satellite operators go to market. Integrating cloud infrastructure with fiber and satellite access networks results in one access layer in a software defined network managed from a single control tier. The satellite operator that can offer this integrated experience commands dramatically higher value than one selling standalone capacity.

Speed to market is an underappreciated dimension of this transformation. Legacy satellite service development cycles were often measured in years. Cloud native architectures compress many of these timelines dramatically resulting in a new analytics service that can be prototyped using existing satellite data streams and cloud processing tools, tested with pilot customers, and scaled commercially in a fraction of the time that would have been required just a few years ago.

4. AI and machine learning enter

The fourth and perhaps most transformative dimension of these partnerships is the integration of artificial intelligence and machine learning into satellite data pipelines. Satellite operators generate enormous volumes of data from the radio frequency environment, telemetry, Earth observation imagery, and usage analytics. For most of the industry’s history, the majority of this data was either ignored or processed manually at great expense and delay. Cloud AI platforms change this approach entirely and do so by employing the following:

Remote sensing intelligence

Automated analysis of Earth observation imagery for applications including crop yield estimation, infrastructure monitoring, and illegal fishing detection.

Predictive logistics

Real-time tracking and routing optimization for maritime and aviation clients powered by satellite AIS and ADS-B data processed through ML models.

Anomaly detection

Automated identification of unusual patterns in satellite telemetry enabling predictive maintenance and reducing costly in orbit failures.

Spectrum management

AI assisted interference detection and frequency optimization improving efficiency across increasingly congested orbital paths.

The strategic implication is significant given that an operator who can offer an AI powered outcome maintains an entirely different position in the value chain than one who offers raw data or connectivity. The former commands subscription revenues with high switching costs while the latter competes primarily on price.

General outlook

The satellite/cloud convergence is a structural response to genuine competitive pressure brought about by the growth of low cost LEO constellations compressing GEO capacity pricing, the rise of enterprise customers who demand software defined network management, and the availability of cloud economics that make new business models financially viable for the first time.

Operators who approach these partnerships strategically by integrating cloud capabilities into their core product roadmaps stand to emerge with strong positions in high growth verticals. Those who treat cloud partnership as a cost exercise while their competitors build data service portfolios risk finding themselves permanently repositioned as simple commodity infrastructure providers.