The Silicon Valley Migration: The Rise of U.S. Micro-Cores

The Silicon Valley Migration: The Rise of U.S. Micro-Cores

U.S. venture capital has increasingly been concentrating in locations outside Silicon Valley

The Silicon Valley Migration: The Rise of U.S. Micro-Cores

For decades a 70+ square mile corridor in Northern California was the undisputed center of technological gravity. Today that core is still there, but the inherent pull unique to the location itself has changed in numerous ways.

The story of American tech in the 2020s isn’t a tale of Silicon Valley’s collapse. It’s something more subtle and interesting in that it is characterized by diffusion. Driven by sky-high housing costs, a substantial increase remote work, and a generation of founders who grew up knowing that great ideas can happen anywhere, a constellation of new tech ecosystems has taken root across the United States. These locations had a fair amount of infrastructure in place and have utilized their inherent advantages to produced spirited environments that are often more specialized and increasingly capable of standing on their own.

Why People Left and Why It Matters

The story begins not with a destination, but with a departure. The Bay Area’s housing crisis has become severe. In Palo Alto, the median home price exceeds $1.5 million, making homeownership unattainable for many. Homelessness has continued to rise, with the Bay Area reporting nearly 39,000 homeless individuals in 2024 which represents a 6% increase from previous years. That pressure, combined with the shift brought about by pandemic driven remote work, created conditions ripe for an exodus. Tech professionals value flexibility and financial freedom, and out of office arrangements allow them to work for companies of varied sizes and funding stages from the comfort of mid to small size cities. These locations can offer a much lower cost of living and lifestyle that may be far more agreeable. Organizations are also concerned about commercial real estate costs and the stringent regulatory environment in California which can induce tremendous difficulties for smaller and mid-size firms.

But here’s where the narrative gets more nuanced: the Bay Area didn’t die. Silicon Valley startups absorbed $90 billion of the $178 billion deployed to U.S. companies in 2024, representing 57% of all domestic venture capital which is the highest concentration since 2018. The dispersion didn’t drain the source, it effectively duplicated it.

The Hubs Taking Shape

Austin: The Flagship Micro-Core

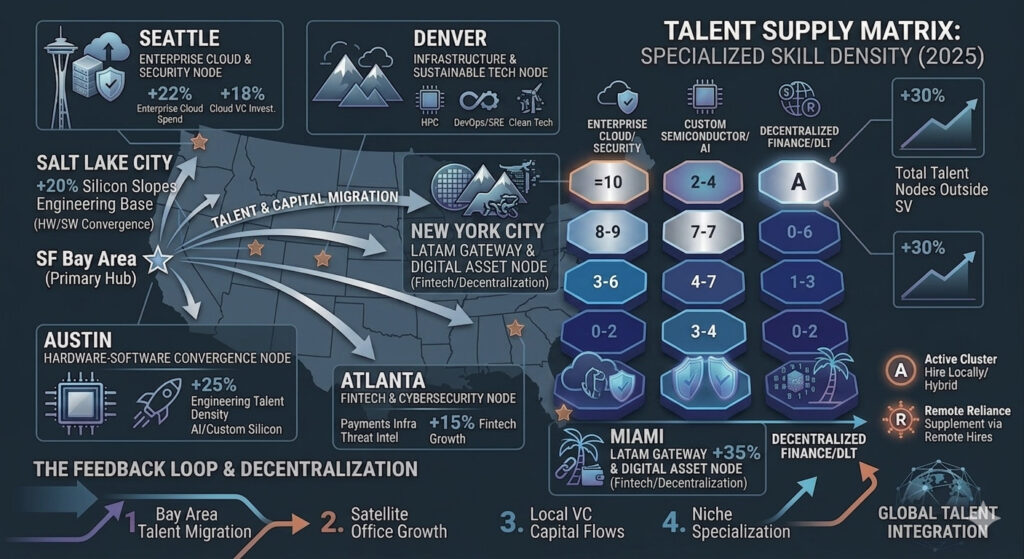

No city better encapsulates the Micro-Core phenomenon than Austin. The city’s startup scene exploded during the pandemic as Bay Area talent relocated for lower costs and business friendly policies. Tesla’s headquarters move in 2021 was certainly a harbinger of what was to come. The city has since developed a talent density that investors recognize as genuinely strong.

The results are now measurable in billions. Investment into area startups spiked 64.8% to $7.19 billion in 2025 compared with $4.37 billion in 2024. This topped even the $6.1 billion raised in 2021 at the height of the venture funding frenzy. The city’s 20 current unicorns are collectively valued at over $54 billion. Strength has been shown in categories such as software, fintech, health tech, defense, energy, and robotics.

New York: The Biggest AI Jobs Market That Was Perhaps Slightly Unexpected…

Silicon Valley still produces the most AI companies, but it’s no longer where the majority of AI workers are being hired. New York has become the country’s largest AI hiring market by volume, adding more than 15,000 relevant job postings between late 2024 and the end of 2025. Tech workers who leave the Bay Area are most likely to move to this region which may seem counterintuitive at first glance given Manhattan’s own high costs. However, the city’s density of industries, finance, media, and fashion all demanding AI integration have provided a strong impetus for relevant individuals to strongly consider this location as a home base.

Miami: Built on a Different Foundation

Miami’s tech emergence follows a different trajectory, driven by cryptocurrency adoption and climate technology development rather than traditional software. The city’s tech sector grew 28% between 2022 and 2024, with particular strength in blockchain infrastructure, decentralized finance, and climate resilience technologies.

The climate angle is especially compelling given rising sea levels and hurricane intensification that create immediate demand for resilience solutions, flood prediction systems, and sustainable infrastructure offerings. Companies developing these technologies benefit from testing in live conditions facing genuine climate threats. Miami isn’t just a place where tech workers moved, it’s a locale where geography itself created a market.

The Research Triangle: The University-Driven Model

The Research Triangle region continues to grow as a tech hub thanks to its three major research universities – Duke, UNC, and NC State – and the Research Triangle Park, one of the largest of these type of locations in the world. Tech professionals enjoy average salaries around $110,000 while benefiting from a cost of living approximately 40% lower than San Francisco, creating one of the best salary to cost ratios for tech workers in the country.

Silicon Slopes: Salt Lake City’s Quiet Ascent

Salt Lake City has quietly built one of the nation’s most dynamic tech scenes. Fueled by ambitious entrepreneurs, low taxes, and a collaborative culture, the city thrives in industries like SaaS, fintech, and biotech, with giants such as Adobe and Oracle having set up major operations here.

The Cost Equation

The most powerful force behind this dispersion is elementary math. A software engineer earning $200,000 in San Francisco faces a median home price multiples of that number makes ownership a decade-long aspiration at best. The same salary in Austin, Denver, or Raleigh-Durham puts ownership within reach in a few years.

At the city level, the situation is extreme. Los Angeles, San Jose, Long Beach, San Francisco, and San Diego all top the list of cities with the highest home price-to-income ratios, ranging from 9.6 to 12.2. Against that backdrop, Austin at roughly 5.5 while Raleigh-Durham is under 4.5. For early-career individuals just out of school, the calculus is increasingly obvious.

What Makes a Micro-Core Thrive?

Not every city that tried to become the next Silicon Valley has succeeded. Miami had a moment of hype in 2021 that was a bit overstated and some of the transplants went back. Denver attracted talent but struggled to retain it at the senior levels needed to build generational companies. The Research Triangle has produced strong mid-size ventures but fewer billion-dollar breakouts than its talent pool might suggest.

What separates Micro-Cores that are genuinely compounding such as those in Austin from those still searching for identity? The evidence points to four factors:

A research anchor matters enormously. The Research Triangle has three major universities generating spinouts. Austin has UT Austin increasingly integrating with its startup ecosystem. Salt Lake City benefits from the University of Utah and BYU’s cultures of entrepreneurship and strong STEM output. Ecosystems without a university engine tend to plateau.

Specialization beats generalization. The most successful Micro-Cores aren’t trying to replicate all of Silicon Valley, they’re finding a lane that functions well. Austin is becoming a leader in defense tech and advanced manufacturing. Miami owns crypto and climate resilience. Boston has dominated life sciences for decades. The cities trying to be good at everything tend to be great at nothing.

Anchor company relocations create multipliers. When Tesla moved its headquarters to Austin in 2021, it didn’t just bring jobs, it brought suppliers, vendors, and dozens of engineers who would eventually leave to start companies. The city attracted other major players drawn by lower costs and a business-friendly environment which concentrated enough density to start the self-reinforcing flywheel.

The AI Jobs Wave Is Reshaping the Map Again

A new force is now rewriting the geography: the artificial intelligence hiring boom. The demand for AI talent is so strong that it’s distributing itself differently than the software wave of the 2010s and some unexpected cities are capturing disproportionate shares.

Unlike Silicon Valley, AI in New York represents a smaller share of the city’s overall workforce because the technology sector spans many industries. That’s actually a sign of depth rather than weakness. AI embedded in finance, healthcare, media, and legal services creates more durable demand than other companies operating in the space that live and die by a single funding cycle. Dallas-Fort Worth added more than 6,000 AI jobs across industries including finance, logistics, telecommunications, and enterprise technology which represents a figure that would have been unimaginable a decade ago for a city not traditionally associated with tech.

The Silicon Valley Response Is Focused On Reinvention

It would be a mistake to read all of this as a permanent decline for the region. While The Bay remains the world’s top tech hub, emerging ecosystems are reshaping the innovation landscape signaling a shift toward a more decentralized global innovation network. The region is, by many measures, doubling down on what it does better than anyone else – frontier AI research, foundation models, and the kind of long-duration, capital-intensive moonshots that require a density of talent and investor sophistication that no Micro-Core has yet replicated.

What’s changed is the market dominance that was in place. The implicit assumption of the 2000s was that if you wanted to build something serious you had to be in the SF area. This has been essentially retired. Innovation ecosystems emerge from landmark technological innovations, and what separates Silicon Valley from other innovation hubs is the speed by which things get done. That advantage is real. But for a growing class of founders building in verticals like defense tech, climate, life sciences, or enterprise SaaS, proximity to deep domain expertise now matters more than closeness to Sand Hill Road.

What Comes Next

The Micro-Core story is still in its early chapters. A few things seem likely to shape the next decade. Remote work norms will continue to evolve, probably settling somewhere between the 2019 default (everyone in the office, everyone in San Francisco) and the 2021 experiment (everyone remote everywhere). That equilibrium will continue to benefit cities that offer the combination of in-person energy and affordable real estate.

The AI buildout will create entirely new geographic concentrations. Data centers and chip fabs require land, power, and water which are resources the Bay Area doesn’t have in abundance. Companies now require a combination of technology, acreage for manufacturing facilities, and talent for pertinent tasks. The physical infrastructure of the AI economy will be built in places that can actually host it.

Perhaps most importantly, a generation of founders who built their companies outside Silicon Valley are now flush with capital and experience and they’re staying put.

The Micro-Cores aren’t replacing Silicon Valley, they’re doing something arguably more significant – proving that the ingredients for world-class innovation can be cultivated almost anywhere.