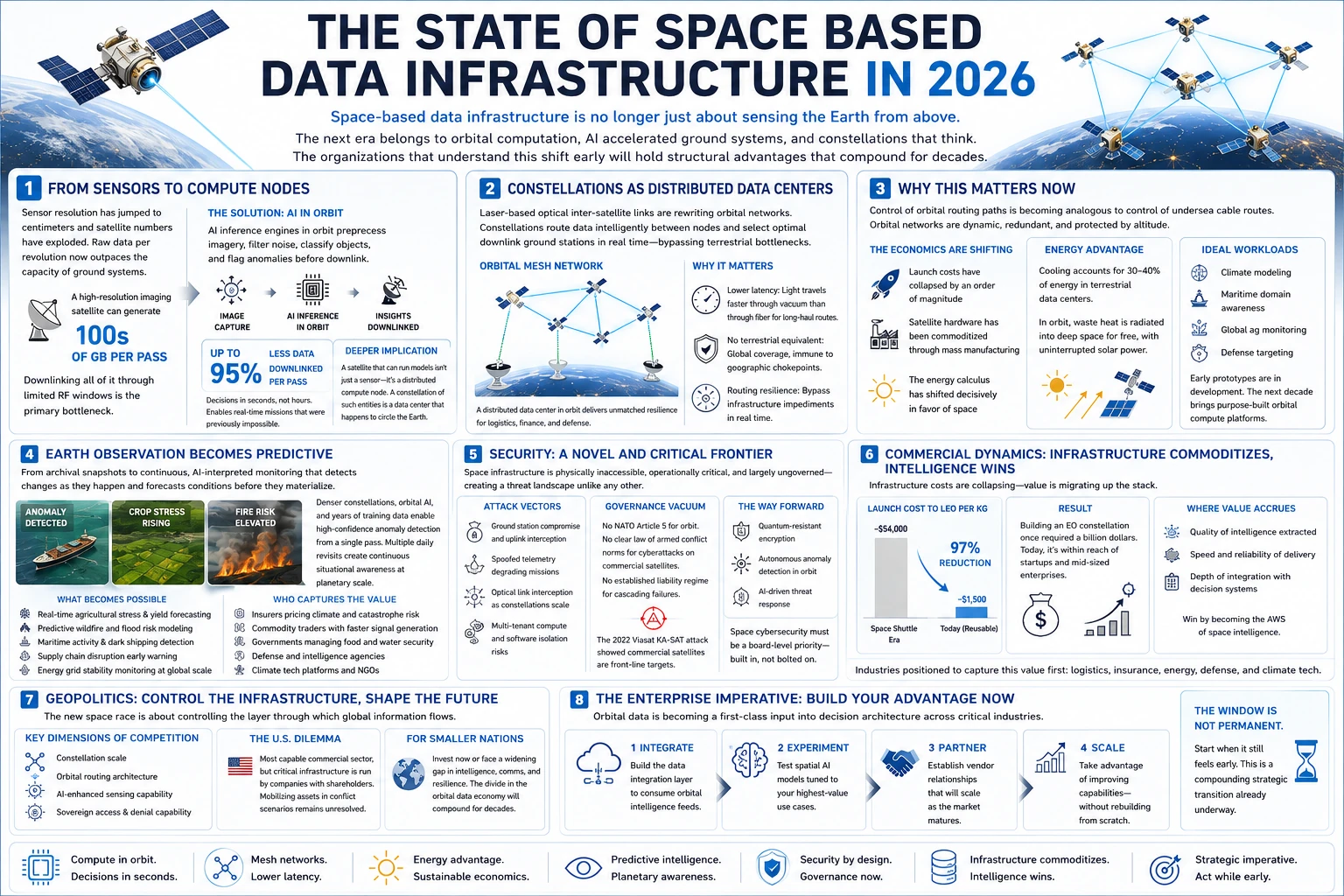

The State of Space Based Data Infrastructure in 2026

The State of Space Based Data Infrastructure in 2026

Space-based data infrastructure is no longer just about sensing the Earth from above

The next era belongs to orbital computation, AI accelerated ground systems, and constellations that think. The organizations that understand this shift early will hold structural advantages that compound for decades.

From sensors to compute nodes

For decades, the satellite’s job was relatively simple – point a camera at Earth, beam the data down, and let ground systems analyze it. That model is rapidly shifting as sensor resolution has jumped from meters to centimeters, and as the number of satellites in orbit has exploded, the volume of raw data generated per revolution has outpaced the capacity of ground infrastructure to effectively absorb it.

The physics of the problem are often difficult at best. A high-resolution imaging satellite can generate hundreds of gigabytes per pass. Downlinking all of it through limited radio frequency windows to a finite number of ground stations across congested spectrum is increasingly the primary bottleneck.

The next iteration of solutions solves this by embedding AI inference engines directly in orbit. Satellites preprocess imagery, filter noise, classify objects, and flag anomalies before the information hits the ground. Only the extracted intelligence gets transmitted. The result is up to 95% less data downlinked per pass, decisions made in seconds rather than hours, and entirely new mission types that real time latency constraints previously made impossible.

The deeper implication is architectural as a satellite that can run models isn’t just a sensor, at that point it’s a distributed compute node. A constellation of such entities coordinating in orbit starts to look less like a camera array and more like a data center that happens to circle the Earth.

Constellations as distributed data centers

Laser based optical inter satellite links are quietly rewriting how orbital networks behave. Instead of isolated platforms that each maintain their own ground contact window, constellations are becoming mesh networks that route data intelligently between nodes, selecting optimal downlink ground stations in real time and bypassing terrestrial bottlenecks entirely for certain intercontinental routes.

The latency implications are significant. Light travels faster through the vacuum of space than through fiber optic glass thus for long-haul routes orbital mesh networks can offer lower end-to-end latency than the best terrestrial backbone. What’s coming next is a more deliberate exploitation of that physics advantage for enterprise and defense applications where milliseconds matter.

Perhaps more consequentially, this architecture transforms constellations into something with no terrestrial equivalent and produces a distributed data center that is simultaneously global in coverage, immune to geographic chokepoints, and capable of routing around physical infrastructure impediments. For logistics, finance, and defense, it’s a resilience capability that terrestrial systems cannot replicate.

Why this matters now

Control of orbital routing paths is becoming analogous to control of undersea cable routes in the 20th century in that whoever owns the infrastructure sets the terms. The difference is that undersea cables are fixed, mappable, and physically severable. Orbital mesh networks are dynamic, redundant, and protected by altitude. The geopolitical implications of this asymmetry are only beginning to be understood.

The idea of processing workloads in orbit has been promoted for decades without gaining traction, largely because the economics never fully made sense. That is rapidly changing due to three primary forces.

• Launch costs have collapsed by an order of magnitude

• Satellite hardware has been commoditized through mass manufacturing

• The energy calculus has shifted decisively in favor of space

Thermal management is one of the least discussed but most significant cost drivers in terrestrial data centers as many estimates suggest cooling accounts for 30–40% of total energy consumption. In orbit, waste heat can be radiated directly into the cold of deep space, effectively for free. Combine that with uninterrupted solar generation above the atmosphere and the operational energy economics of an orbital data center start to look competitive with ground based alternatives for specific workload classes.

These tasks best suited for orbital compute tend to share a common characteristic in that they require a true planetary vantage point. Climate modeling, maritime domain awareness, global agricultural monitoring, and defense targeting for example are applications where the data is inherently global, continuous, and time sensitive. Sending it to Earth for processing only to route intelligence back up introduces latency and single points of failure that orbital compute eliminates by design.

Early prototypes are already in development and the next decade will see orbital compute evolve from experimental payloads to purpose built platforms designed to handle workloads that have no terrestrial equivalent.

Earth observation becomes predictive

The traditional model of Earth monitoring is archival as a satellite passes overhead, captures an image, and analysts examine it hours or days later to understand what was happening at a given moment. That construct is giving way to something fundamentally different entailing continuous, AI interpreted monitoring that flags changes as they occur and forecasts conditions before they materialize.

What makes this possible is the combination of denser constellations, orbital AI inference, and the accumulation of long training datasets. Machine learning models coached on years of historical imagery can now detect anomalies (a ship behaving unusually, a field greening faster than expected, a power grid fluctuating) with high confidence from a single pass. Stacked across a constellation making multiple daily revisits, this becomes continuous situational awareness at planetary scale.

What becomes possible

• Real-time agricultural stress and yield forecasting

• Predictive wildfire and flood risk modeling

• Maritime activity and dark shipping detection

• Supply chain disruption early warning

• Energy grid stability monitoring at global scale

Who captures the value

• Insurers pricing climate and catastrophe risk

• Commodity traders with faster signal generation

• Governments managing food and water security

• Defense and intelligence agencies

• Climate tech platforms and NGOs

Security

Space-based infrastructure introduces a threat surface that is genuinely novel, physically inaccessible, operationally critical, and largely ungoverned. The combination creates security conditions unlike anything facing terrestrial IT or even undersea cable infrastructure.

The attack vectors are multiple and asymmetric. Ground station compromise remains the most accessible entry point as a sophisticated adversary doesn’t need to strike a satellite in orbit when it can intercept or corrupt the uplink. Spoofed telemetry can silently degrade mission performance without triggering obvious alerts. Inter satellite optical links, while harder to intercept than radio frequency communications, introduce new attack surfaces as constellations scale. And as orbital compute matures, the prospect of multi-tenant environments in space raises software isolation concerns that the cloud industry spent a decade learning to manage and is still getting wrong on the ground.

The governance vacuum compounds the technical challenge. There is no equivalent of a NATO Article 5 commitment for orbital infrastructure, no universally recognized law of armed conflict norms for cyberattacks on commercial satellites, and no established liability regime for cascading failures caused by a compromised constellation. The 2022 attack on Viasat’s KA-SAT network which disrupted satellite communications across Europe hours before Russia’s invasion of Ukraine demonstrated that commercial satellite infrastructure is now a front line military target. The legal and strategic frameworks haven’t caught up.

Quantum resistant encryption, autonomous anomaly detection running in orbit, and AI driven threat response are the technical directions the industry appears to be moving. However, the more difficult problem is organizational as space cybersecurity needs to become a board level priority that is integrated into procurement decisions, not retrofitted after deployment.

Commercial dynamics

For most of its history, space was a domain defined by scarcity including launch capacity, available orbital slots, engineering talent, and a lack of capital investors willing to accept decade long development timelines. All of that is changing and the pace is compressing in ways that are difficult to fully appreciate.

The cost to launch a kilogram to low Earth orbit has fallen from roughly $54,000 in the Space Shuttle era to under $1,500 today with reusable vehicles which represents a 97% reduction in four decades – the steepest drop being seen in the last ten years. Mass manufactured satellite platforms, modular payload architectures, and software defined radio and imaging systems have reduced per unit hardware costs by comparable magnitudes. The net effect is that building and launching a capable Earth observation constellation, which required a sovereign space program or a billion dollar commercial venture a decade ago, now sits within reach of well funded startups and mid sized enterprises.

This commoditization creates a dynamic very familiar from cloud computing in that as infrastructure costs collapse, the value migrates up the stack. This trajectory mirrors the evolution of cloud computing. AWS didn’t win by having the best servers. It prevailed by abstracting infrastructure into an accessible API and letting the ecosystem build on top of it. The orbital data companies that win the next decade will be those that become the AWS of space intelligence by being reliable, programmable, deeply integrated, and easy to build on.

The differentiator here won’t be owning satellites but, rather, the quality of the intelligence extracted from their data, the speed and reliability of delivery, and the depth of integration with downstream decision systems. The industries positioned to capture this worth first are those with the highest tolerance for novel data sources and the clearest use case for planetary scale situational awareness such as logistics, insurance, energy, defense, and climate tech.

Geopolitics

The space race of the 21st century looks nothing like the one of the past 100 years. It is about controlling the infrastructure layer through which global information flows and the economic and military leverage that comes with that oversight. Countries are now competing across several distinct dimensions simultaneously including constellation scale, orbital routing architecture, AI enhanced sensing capability, and the sovereign capacity to deny adversaries access to space derived intelligence.

The United States faces a genuinely complex strategic situation as its commercial space sector is the most technically capable in the world, but the diffusion of this prowess to private actors means that critical national security infrastructure is operated by companies with shareholders. The debate over how to mobilize commercial orbital assets in a conflict scenario (and who gets to make crucial decisions) is far from resolved.

For smaller nations, the calculus is equally stark. Those that invest now in either sovereign orbital capability or preferential access agreements with leading constellation operators will have qualitatively different intelligence and communications capabilities than those that don’t. The gap between supported and underserved nations in the orbital data economy will widen, with downstream consequences for economic development, climate resilience, and security that compound over decades.

The enterprise imperative

For most ventures, space remains a niche data source used by specialists in often rather narrow verticals. The organizations building durable advantages in logistics, insurance, energy, and agriculture are treating orbital data as a first class input into their decision architecture.

The practical starting point isn’t launching satellites. It’s building the data integration layer to consume orbital intelligence feeds, experimenting with spatial AI models tuned to specific use cases, and establishing vendor relationships that will scale as the market matures. The companies investing in that foundation now will be able to take advantage of improvements in orbital capability (more frequent revisits, higher resolution, faster inference, lower cost) that are coming in the next five years without having to rebuild from scratch each time.

The window for building this advantage in orbital data strategy is not permanently open. As costs fall and capabilities improve, the gap between early adopters and late movers will close in capability but may not fully shut with regard to institutional knowledge, vendor relationships, and embedded workflows. The time to start is when it still feels early and recognize this shift as a compounding strategic transition already underway.