The Rise of Vertical SaaS Ecosystems and How They’re Changing Partnership Strategy

The Rise of Vertical SaaS Ecosystems and How They’re Changing Partnership Strategy

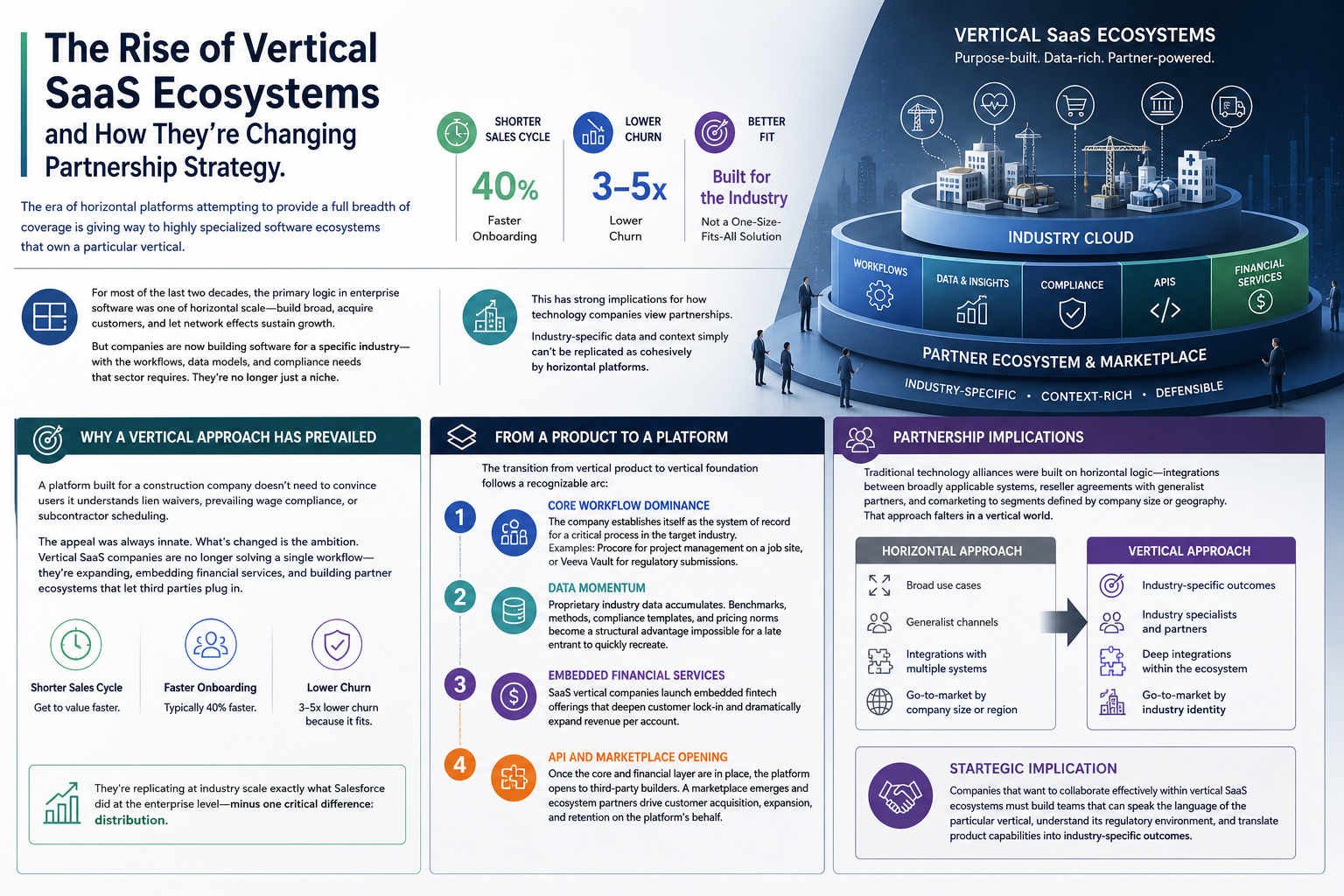

The era of horizontal platforms attempting to provide a full breadth of coverage is giving way to highly specialized software ecosystems that own a particular vertical

For most of the last two decades, the primary logic in enterprise software was one of horizontal scale which entailed building a platform sufficiently broad, acquiring enough customers to properly fuel it, and allowing the subsequent network effects to sustain growth. However. there has been a tangible shift in recent years where companies are constructing software intended for a specific industry that contain workflows, data models, and compliance needs of that particular sector. This has strong implications for how technology companies view partnerships.

Why a vertical approach has prevailed

The appeal of this form of SaaS was always somewhat innate as a given type of platform built specifically for a construction company, for example, doesn’t need to spend years convincing its users that it can fully address items such as lien waivers, prevailing wage compliance, or subcontractor scheduling. Given this, the sales cycle is shorter, onboarding is faster (typically 40%), and churn is 3 to 5 times lower because the product fits like it was indeed made for this particular function.

What’s changed more recently is the direct determination of vertical SaaS companies. They are no longer content to solve a single workflow problem and are expanding aggressively while absorbing adjacent functionality, embedding financial services, and building out partner ecosystems that let third-party software plug in.

In doing so they are replicating at industry scale exactly what Salesforce did at the enterprise level minus one critical difference – distribution. Industry specific data and context simply can’t be replicated as cohesively by horizontal platforms.

The transition from vertical product to vertical foundation is the defining strategic move of this era. It typically follows a recognizable arc:

From a product to a platform

Core workflow dominance

The company establishes itself as the system of record for a critical process in the target industry. Procore for project management on a job site, or Veeva Vault for regulatory submissions are good examples.

Data momentum

As more customers use the platform, proprietary industry data accumulates. Benchmarks, methods, compliance templates, and pricing norms all become data that forms a structural advantage impossible for a late entrant to quickly recreate.

Embedded financial services

SaaS vertical companies are increasingly launching embedded fintech offerings that deepen customer lock in and dramatically expand revenue per account.

API and marketplace opening

Once the core and the financial layer are in place, the platform opens to third party builders. A marketplace emerges and ecosystem partners begin to drive customer acquisition, expansion, and retention on the platform’s behalf.

Partnership Implications

Traditional technology alliances were built on horizontal logic where integrations between broadly applicable systems, reseller agreements with generalist channel partners, and comarketing to shared customer segments defined by company size or geography was the primary route to success. However, this approach tends to falter when the central platform is vertical as this type of SaaS ecosystem is organized around industry identity rather than company profile.

Strategic implication

Companies that want to collaborate effectively within vertical SaaS ecosystems must build teams that can speak the language of the particular vertical, understand its regulatory environment, and translate product capabilities into industry specific outcomes.

Five ways vertical SaaS is rewriting partnership strategy

Platform owner dynamics replace peer-to-peer relationship

When you integrate with a vertical SaaS platform that owns the system of record, you’re not negotiating between equals. This is an ecosystem where the platform controls access to customers, data, and distribution thus partnership terms, data sharing rights, and marketplace positioning are set by the platform owner. This means that the balance of power is rarely symmetric thus savvy partnership teams take an open approach and invest in building genuine value for customers.

Partner selection becomes highly industry specific

The days of a single partner agreement covering multiple verticals are numbered. A compliance workflow tool predominant in healthcare is now often irrelevant in hospitality. Partnership portfolios need to be curated by vertical, and the partner success view needs to reflect the specific integration surface, buyer persona, and workflow context of each industry the platform serves.

Embedded fintech creates new partnership categories

As vertical SaaS companies layer in payments, insurance, and lending, they open up new partnership opportunities with financial services providers. A construction platform offering contractor financing requires very different partners than it did when it was purely a project management tool. ISOs, lenders, insurers, and card networks are increasingly showing up in partner ecosystem conversations that would have been purely software to software only a few years ago.

Data sharing agreements become the critical negotiating key

The value of integrating with a vertical platform is often less about the functionality it unlocks and more about the data it unearths. Industry specific usage patterns, workflow benchmarks, and customer cohort data can be enormously valuable for product development and market push, but vertical SaaS platforms protect this diligently for good reason. Negotiating data access rights, API rate limits, and customer consent frameworks is increasingly where partnership deals are found.

Co-selling requires vertical credibility along with customer knowledge

When your field team joins a customer call with a vertical SaaS platform’s account executive, the client is not just evaluating the product integration. They want to know if your group understands their particular realm. Building vertically credible sales and partner success organizations is a competitive differentiator in ecosystem selling.

Looking forward

We are likely approaching an inflection point in vertical SaaS and this is readily apparent with a number of companies that we are currently working with. The first generation of category defining platforms are now mature enough to have clear ecosystem strategies and the market leverage to effectively employ them. The second iteration of these ventures are still in the platform building phase, seeking integrations and willing to offer favorable partnership terms to attract quality ecosystem collaborators early in the process.

Given this, technology companies evaluating their vertical SaaS partnership strategy have a great deal of understood urgency. The window to establish preferred partner status in a growing vertical ecosystem is most opportune at this stage. Once a vertical platform reaches critical mass the economics of ecosystem participation almost inevitably shift materially toward the platform owner.

The companies that will succeed in this environment are those that treat this vertical approach as an industry relationship to be invested in rather than a distribution channel to be managed.