Why Venture Capital Is Rediscovering Physical Products

Why Venture Capital Is Rediscovering Physical Products

For most of the past decade, the prevailing wisdom in venture capital was remarkably consistent.

Software was often the only game worth playing as the margins were extraordinary, the distribution was global, and the capital requirements were modest by comparison to anything that required a factory, a supply chain, or a bill of materials. The phrase “hardware is hard” became something of a mantra and investors who strayed into physical products were often viewed as contrarians at best.

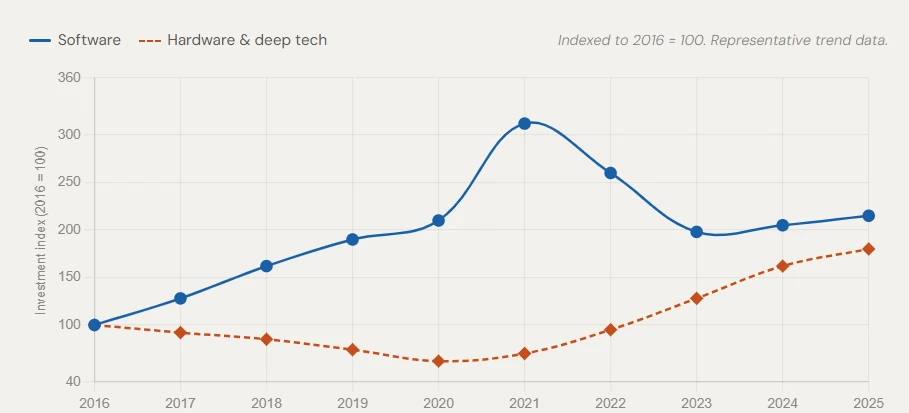

That consensus is now breaking down in a meaningful and accelerating way. Hardware investment is making a marked comeback, and the reasons behind it are both structural and strategic. Understanding what is driving this shift matters to anyone who builds, funds, or recruits in the technology sector.

The Software Premium Has Limits

The SaaS model produced extraordinary returns and, in doing so, attracted enormous amounts of capital. Valuations expanded well beyond traditional multiples, and by the early part of this decade a significant portion of the software landscape had become genuinely crowded. Differentiation grew harder to establish and even more difficult to sustain. When every company in a given category offers broadly similar capabilities at relatively similar price points, the competitive advantage tends to migrate away from the product itself and toward distribution, brand, and customer relationships.

That can be a defensible position, but it is not a particularly exciting one for investors looking for the next substantial return. The search for categories with unique attributes has led a growing number of funds back toward physical products. The supply chain knowledge, manufacturing relationships, regulatory compliance, and iterative engineering required to bring a physical product to market are not trivially replicated by a well-funded competitor.

|

Software |

Hardware |

|

|---|---|---|

|

Replication speed |

Fast – weeks to months |

Slow – years of iteration |

|

Gross margin profile |

70 – 90% |

30 – 60% |

|

Primary moat |

Data network effects, switching cost |

Supply chain, IP, regulatory approval |

|

Distribution complexity |

Low – cloud/digital channels |

High – logistics, service, support |

|

Capital intensity |

Low to moderate |

High – offset by grants and CVC |

|

Talent scarcity |

Competitive |

Acute – specialist engineers are scarce |

AI Changed the Hardware Calculus

Perhaps the single most important factor in the renewed interest in hardware is the rapid maturation of artificial intelligence and the infrastructure required to run it. Simply put, AI is not an abstraction that lives entirely in the cloud. It runs on chips, in data centers, across specialized networking equipment, and increasingly on edge devices that sit in factories, vehicles, and clinical settings. The demand for processors/chips, advanced cooling systems, power delivery infrastructure, and robotics capable of operating in complex physical environments has created an entirely new market for hardware companies. Investors who would have more than likely passed on a hardware deal five years ago are now actively seeking founders who can effectively operate in this space.

Defense and National Security Considerations

The geopolitical environment has added another dimension to the hardware conversation that would have seemed peripheral to many investors just a few years ago. The vulnerability of global supply chains, the concentration of advanced semiconductor manufacturing in a small number of geographic locations, and the growing recognition that strategic technologies should not be entirely dependent on foreign production have all created policy incentives and institutional demand for domestic hardware capability.

Primary defense companies, national laboratories, and government agencies are all spending in ways that provide meaningful revenue to hardware firms at early stages of development. For investors, this creates a more favorable funding environment than hardware typically enjoyed. A company with a credible defense application and a meaningful contract has a cleaner path to sustained revenue than a consumer hardware startup dependent on retail distribution and mass market adoption. The combination of government demand and commercial potential is attractive in a way that was less common before recent shifts in policy priorities.

The Robotics Factor

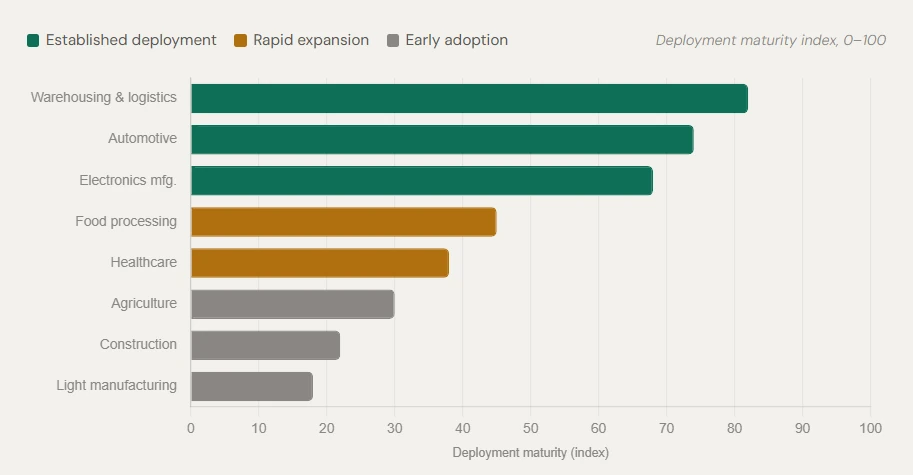

Robotics deserves particular attention as a category that has moved from peripheral curiosity to serious investment target in a relatively short period of time. The underlying enabling technologies, including vision systems, large language models capable of interpreting instructions in natural language, improved actuators, and more capable planning algorithms, have all advanced to the point where these systems are now genuinely useful in a broad range of commercial settings.

Warehousing and logistics were the first large sectors to employ significant robotic deployment, but the pattern is now extending into agriculture, construction, healthcare, and light manufacturing. Each of these markets is large, and the total cost of robotic ownership has declined substantially as the underlying components have matured. Investors who were skeptical of this category are finding it harder to dismiss the combination of capability, market size, and urgency that currently exists.

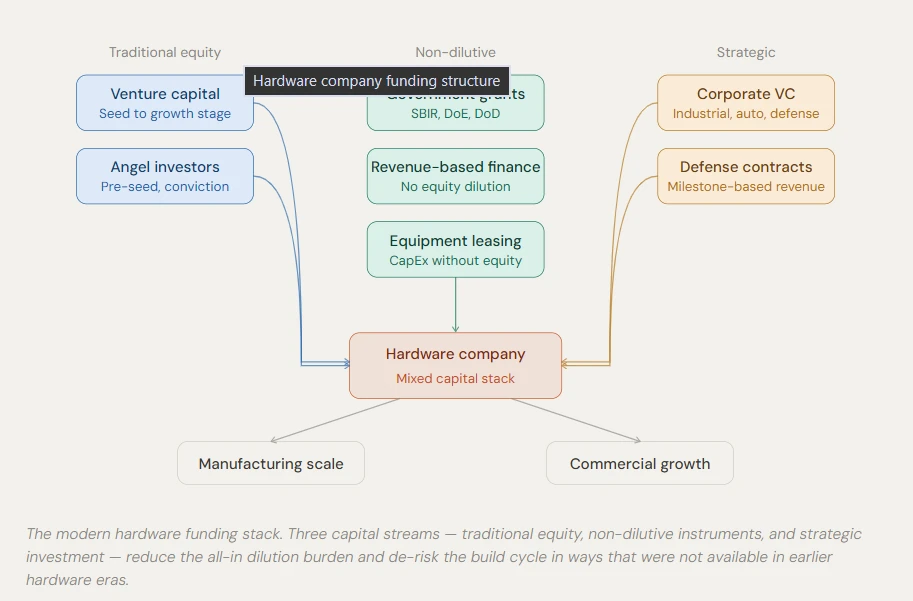

What Changed in the Funding Environment

Several structural developments have made hardware more viable as an investment category. The growth of non-dilutive financing options, including revenue based financing, equipment leasing, and government grants tied to manufacturing and clean energy objectives, means that hardware companies no longer need to absorb the full capital intensity of their build cycle through equity alone. This changes the math in ways that make early stage hardware more appealing to founders and investors simultaneously.

Corporate venture capital has also played a meaningful role. Large industrial companies, automotive manufacturers, and defense contractors all operate venture arms that have strategic as well as financial motivations. These investors bring distribution relationships, customer access, and technical credibility that a purely financial investor simply cannot provide. The presence of a strategic co-investor can significantly reduce the amount of risk attendant to a hardware deal in ways that are specific to the category.

Finally, the cohort of hardware founders who came through the consumer electronics era, the clean technology boom, and the first wave of industrial robotics companies has matured. There is now a much larger pool of experienced operators who know how to manage supply chains, negotiate with contract manufacturers, navigate regulatory processes, and scale physical production. That type of knowledge makes hardware investing more straightforward than it was when the category was younger and the experienced operator base was smaller.

The Talent Dimension

Any discussion of the hardware resurgence has to include the talent question, because hardware companies face recruiting challenges that are categorically different from software companies. The engineers who design custom silicon, build firmware for constrained environments, and understand the physics of power electronics or the chemistry of battery systems, are genuinely scarce. The current surge in demand, and the combination of AI infrastructure buildout, defense investment, and commercial robotics expansion has made them considerably more so.

The organizations that will benefit most from the present hardware investment cycle are those that treat talent acquisition with the same rigor they apply to product development. Identifying the specific technical and leadership profiles required, building relationships in communities where that talent concentrates, and moving quickly when the right candidate is available are essential.

What the Resurgence Signals

The return of serious venture capital to hardware is not a rejection of software or a nostalgic turn toward an earlier model of technology investment. It’s a recognition that the most consequential technology problems of the current era require solutions that exist in both the digital and physical domains simultaneously. The companies that can operate credibly in both (and the investors who can evaluate and support them) are positioned well for what comes next.

Renascent Solutions Venture Capital | Private Equity Recruitment