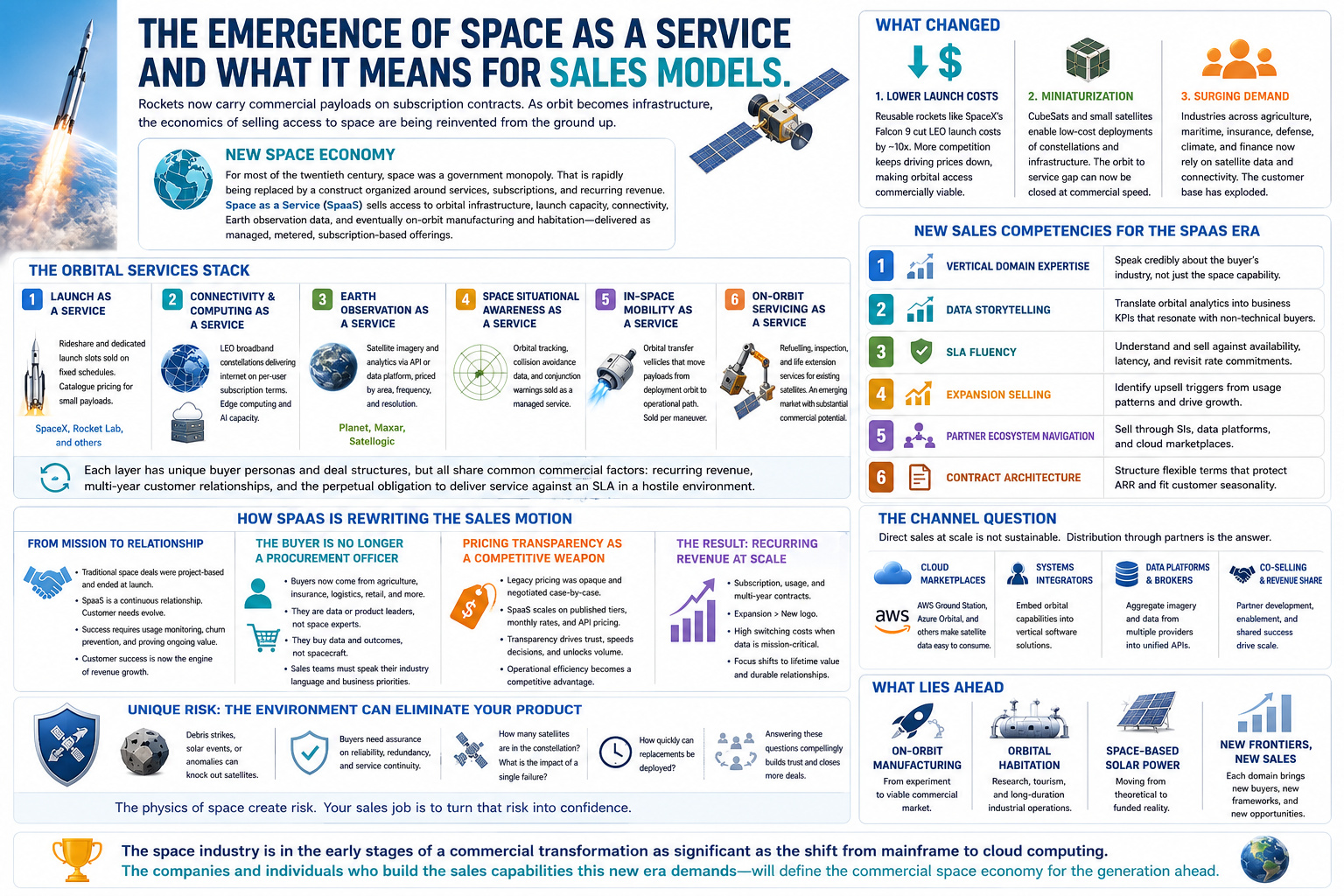

The Emergence of Space as a Service and what It Means for Sales Models

The Emergence of Space as a Service and what It Means for Sales Models

Rockets now carry commercial payloads on subscription contracts. As orbit becomes infrastructure, the economics of selling access to space are being reinvented from the ground up.

New space economy

For most of the twentieth century, space was a government monopoly. Economics were essentially irrelevant because the customer was the public sector. Commerce, if it existed at all, was little more than a footnote. That is rapidly being replaced by a construct organized around services, subscriptions, and recurring revenue.

Space as a Service is now a viable term that would have seemed rather inane not that long ago. It encompasses a model in which access to orbital infrastructure, launch capacity, satellite communications, Earth observation data, and eventually on orbit manufacturing and habitation are sold not as bespoke, one off missions but as managed, metered, subscription based offerings.

What changed

Three forces appear to have created the conditions for SpaaS to become a key player. The first was the dramatic decrease in launch costs. SpaceX’s reusable Falcon 9 reduced the monetary requirements of putting a payload into low Earth orbit by roughly an order of magnitude compared to the legacy expendable launcher era. Competitors inevitably arose, and the price of access to orbit continued its downward trajectory. When launch is cheap enough, commoditized orbital slots become commercially viable.

The second force was miniaturization. Cubesats and small satellites made it possible to deploy functional orbital infrastructure for far less. Constellations became buildable on commercial timelines. A number of new players all demonstrated that the orbit to service gap could be closed at commercial speed and cost.

The third factor was simple demand. Countless industries including agriculture, maritime logistics, insurance, defense, climate science, and financial services discovered that satellite derived data and connectivity had moved to operationally essential. The customer base for orbital services rapidly expanded in scope and diversified in thus selling space was no longer simply a matter of navigating a handful of government procurement offices.

The Orbital Services Stack

Launch as a Service

Rideshare and dedicated launch slots sold on fixed schedules. SpaceX, Rocket Lab, and others now offer catalogue pricing for small payloads

Connectivity and Computing as a Service

LEO broadband constellations delivering internet access globally on per user subscription terms. Edge computing and AI capacity, processing, output

Earth Observation as a Service

Satellite imagery and analytics delivered via API or data platform, priced by area, frequency, and resolution. Planet, Maxar, and Satellogic compete here

Space Situational Awareness as a Service

Orbital tracking, collision avoidance data, and conjunction warnings sold to satellite operators as a managed safety service

In Space Mobility as a Service

Orbital transfer vehicles that move payloads from deployment orbit to operational path. Sold per maneuver

On Orbit Servicing as a Service

Refuelling, inspection, and life extension services for existing satellites. An emerging market with substantial commercial potential

Each of these layers carries different sales dynamics, unique buyer personas, and varying assumptions about what a deal looks like. However, they share common commercial factors including recurring revenue, multi-year customer relationships, and the perpetual obligation to deliver service against an SLA operating in one of the most hostile environments known.

How SpaaS Is Rewriting the Sales Motion

From mission to relationship

Traditional space procurement was project based. A government agency or commercial operator defined a mission requirement, went through a multi-year procurement process, awarded a fixed-price or cost-plus contract to a prime contractor, and then managed that agreement through development to launch. The relationship that followed was largely administrative contract management.

SpaaS compacts are fundamentally different. For example, an Earth observation customer who subscribes to daily coverage of a specific agricultural region is making an ongoing purchasing decision. Their use case evolves as they add more regions, seek higher temporal resolution during growing season, and desire analytics layered on top of raw imagery. The vendor who treats the initial subscription as the endpoint and stops selling is leaving the majority of the customer’s lifetime value on the table.

This structural shift demands a customer success approach that the traditional space industry has never had to construct. Account management in legacy aerospace meant managing contract milestones whereas in SpaaS this requires monitoring usage data, identifying expansion opportunities, intervening before a customer churns over a service degradation event, and continuously demonstrating that the capability being subscribed to is generating measurable business value.

The buyer is no longer a procurement officer

Government space procurement is managed by specialists who understand orbital mechanics, payload requirements, and defense/civil space contracting. They buy infrequently, deliberate slowly, and evaluate vendors through established acquisition frameworks.

SpaaS has dramatically expanded and diversified the buyer universe. An agricultural technology company buying satellite imagery to feed a crop monitoring algorithm is making a data infrastructure decision, not a space decision. The buyer may be a Head of Data Engineering or a VP of Product who typically doesn’t know that they are buying a space product. They are buying a data service.

This transformation in buyer persona requires a shift in sales talent. The engineer salesperson who can masterfully convey a technical conversation about orbital insertion is still valuable, but they cannot be the whole team. SpaaS providers now need salespeople who can walk into a maritime insurance firm, a precision agriculture company, or a retail supply chain operation and translate orbital capabilities into business outcomes their buyers can understand. That requires domain expertise in the customer’s vertical as well as space.

Pricing transparency as a competitive weapon

Legacy space procurement was generally nebulous by design. Prices were negotiated individually, held confidential, and varied enormously based on relationship history, contract volume, and the buyer’s perceived leverage. This opacity suited prime contractors who had proper relationships and protected incumbents from competitive pressure.

SpaaS is forcing transparency. When you are selling connectivity/imagery/computation at scale to thousands of commercial customers, negotiating every contract individually is operationally impossible. Pricing tiers, monthly rates, and API pricing have all come to the forefront.

New Sales Competencies for the SpaaS Era

Vertical domain expertise

Ability to speak credibly about the buyer’s industry, not just the space capability being sold

Data storytelling

Translating orbital analytics into business KPIs that resonate with non-technical buyers

SLA fluency

Understanding and selling against availability, latency, and revisit rate commitments in physical terms

Expansion selling

Identifying upsell triggers from usage patterns and proactively structuring growth conversations

Partner ecosystem navigation

Selling through systems integrators, data platforms, and cloud marketplaces as distribution channels

Contract architecture

Structuring flexible commercial terms that protect ARR while accommodating customer seasonality and demand

The Channel Question

One of the most consequential structural changes SpaaS introduces is the rise of the channel. Direct government sales have always been the primary base of the space industry’s commercial model and incorporated relationships cultivated over years. But serving thousands of commercial customers across dozens of verticals with a direct salesforce is economically unsustainable for most orbital service providers.

The answer, increasingly, is distribution through partners. Cloud hyperscalers who list satellite data products on their marketplaces, systems integrators who embed orbital capabilities into vertical software solutions, and data brokers who aggregate imagery from multiple providers into unified platforms have all seen success. AWS Ground Station, Microsoft Azure Orbital, and Google’s partnerships with Earth observation providers all may be included as examples. For the space companies feeding these platforms, it means utilizing partner development, revenue sharing, co selling, and enabling a channel to sell something they only partially understand.

Unique Risk

SpaaS introduces a unique proposition: the physical environment can eliminate your product. A satellite struck by debris, degraded by a solar event, or experiencing an anomaly on its payload is not delivering its contracted service.

This forces a conversation about reliability, redundancy, and service continuity that most commercial buyers have never had to have before. How many satellites are in the constellation? What is the revisit rate impact of a single spacecraft failure? How quickly can the operator deploy replacements? These are questions that a procurement officer at an insurance firm has no framework for evaluating, and answering them compellingly is one of the defining sales skills of the SpaaS era.

The companies that get this right will build durable competitive advantage. Customers who have integrated satellite data into critical operational workflows do not churn lightly. Customer acquisition cost in SpaaS is high, but so is the switching hit, and the vendors who understand both will price and sell accordingly.

What Lies Ahead

The next wave of SpaaS expansion will move beyond Earth observation and connectivity into domains that are harder to sell but potentially far more transformative. On orbit manufacturing is advancing from experiment to viable commercial market. Orbital habitation, both for research and eventually for tourism and long duration industrial operations, is being built out by multiple providers simultaneously. Space based solar power is moving from theoretical to funded. Each of these categories will require entirely new commercial frameworks, new buyer personas, and new sales capabilities.

The space industry is in the early stages of a commercial transformation as significant as the shift from mainframe to cloud computing. The companies and individuals who build the sales capabilities this new era demands, rather than trying to apply the old government contracting approach, will define the commercial space economy for the generation ahead.