The End of the Seat: How AI Agents Are Rewriting the Rules of Software Pricing

The End of the Seat: How AI Agents Are Rewriting the Rules of Software Pricing

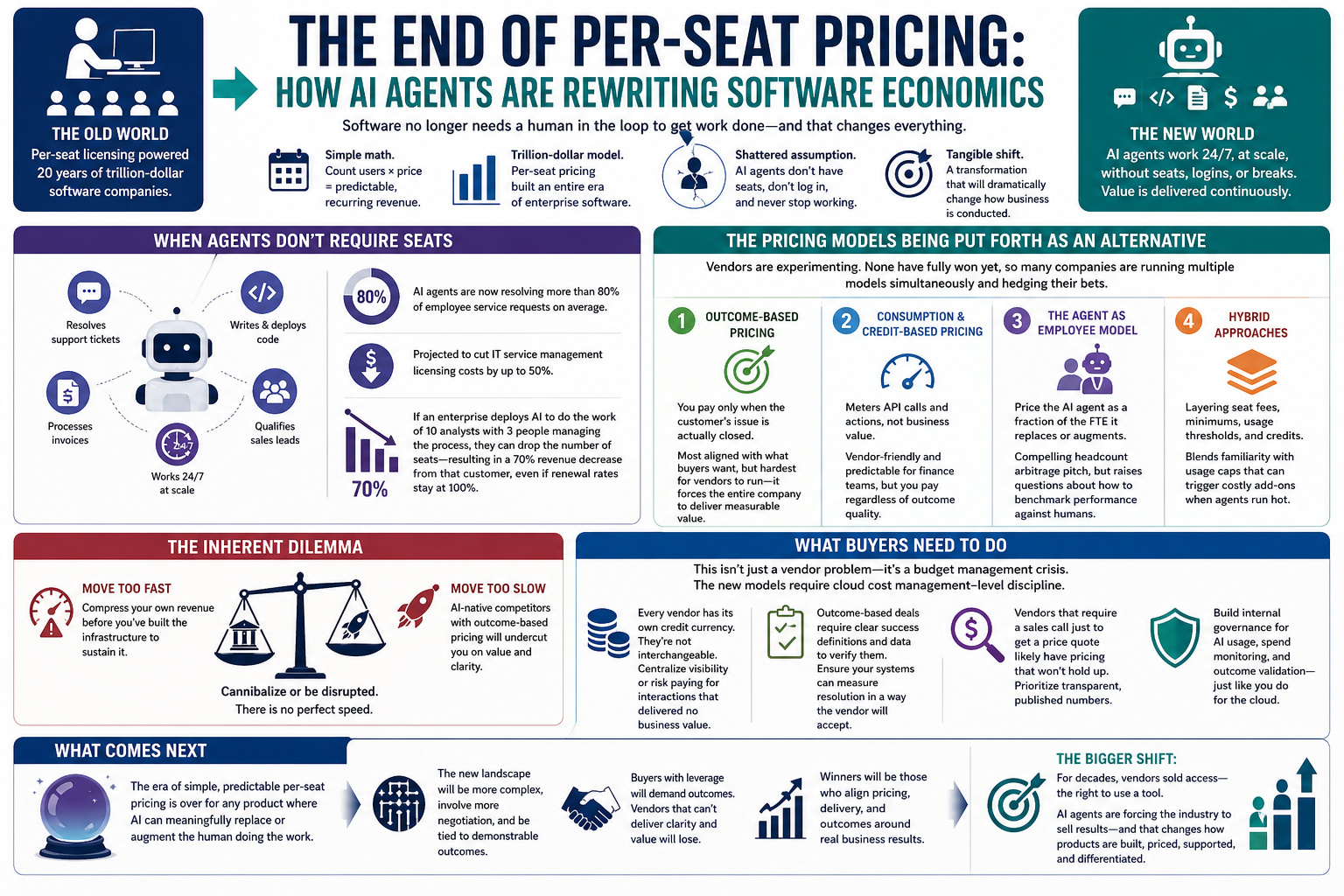

For two decades, the per-seat license was the engine of the software industry…

The math for this type of approach has been quite simple, the contracts were predictable and the revenue was recurring. It was a model that powered an entire era of trillion-dollar companies. That structure is now undergoing a tangible shift if not outright sweeping transformation that will dramatically change how business is conducted. Software no longer needs a human sitting in front of it to get things done.

When agents don’t require seats

The logic of per-seat pricing always rested on the assumption that software is a tool that humans use. You count the users, multiply by the price, and you have your contract. It made sense when every interaction required a person to log in and complete various activities. AI agents shatter that assumption entirely. An autonomous agent doesn’t have a seat, doesn’t have to log in or stop working at a given time. It resolves support tickets, writes and deploys code, processes invoices, and qualifies sales leads on a continuous basis. This can be done at scale without a human attached to each action.

The implications are already being felt. A recent report found that AI agents are now resolving more than 80% of employee service requests on average which represents a shift projected to cut IT service management licensing costs by up to 50%. If an AI is closing this percentage of your CRM tickets, you’re going to want a proportionately less amount of fulfiller seats. If an enterprise deploys AI to do the work of 10 analysts with 3 people involved in managing the process they can effectively drop the number of seats. This will be a 70% revenue decrease from that customer, even if renewal rates stay at 100%.

The pricing models being put forth as an alternative

Software vendors are attempting to respond with overlapping experiments. None of them have fully won yet, and many companies are running multiple models simultaneously and hedging their bets while the market figures itself out.

Pricing models being implemented

Outcome-based pricing

Seems to be the most philosophically aligned with the new reality. You pay only when the customer’s issue is actually closed. It’s the model most aligned with what buyers actually want, but it’s also the hardest for vendors to run as it forces every part of the company to genuinely deliver measurable value.

Consumption and credit-based pricing

Most of the large enterprise players appear to be headed in this direction, at least for now. This model is vendor-friendly as it meters API calls and actions, not business value, so vendors get paid regardless of outcome quality. It’s also predictable enough for enterprise finance teams to plan around.

The agent as employee model

Rather than metering interactions, vendors price their AI agent as a fraction of the full-time employee it replaces or augments. It’s a compelling pitch that reframes software spend as headcount arbitrage, though it raises questions about how you benchmark performance against the human alternative.

Hybrid approaches

Vendors are layering seat fees, platform minimums, usage thresholds, and credit purchases on top of each other in ways that make the total cost of ownership genuinely difficult to calculate. For example, many are blending seat-based and consumption-based pricing so to give procurement teams a familiar cost envelope while embedding usage caps that can require add-ons if agents run hot.

The inherent dilemma

What makes this transition especially treacherous for established software companies is that they have to cannibalize themselves to thrive. Move to outcome-based pricing too fast and you compress your own revenue before you’ve built the infrastructure to sustain it. Move too slowly and AI native competitors who’ve built their pricing around outcomes from day one will undercut you on value and clarity.

What buyers need to do

For enterprise software buyers, the shift to agentic pricing isn’t just a vendor problem, it’s a budget management crisis waiting to happen. The old model was easy to govern: count seats, multiply by price, sign the contract. The new constructs require a fundamentally different discipline that incorporate practices built for cloud cost management.

A few practical realities for procurement teams navigating this environment

Every major vendor now has its own credit currency, and those are not interchangeable or intuitive. Without a centralized view, organizations can easily end up paying for AI interactions that delivered no business value at all. Outcome-based contracts are attractive in theory but require you to define what success actually means and to have the data to verify it. Before signing a deal make sure your systems can actually measure resolution in a way the vendor will accept.

The vendors who require a sales call just to get a price quote are the ones most likely to have pricing that doesn’t hold up to scrutiny. Prioritize vendors with published, transparent numbers as it’s a strong signal they’ve built a model they can defend.

What Comes Next

It’s clear that the era of simple, predictable per-seat pricing is over for any product where AI can meaningfully replace or augment the human doing the work. The new pricing landscape will be more complex, involve more negotiation, and be tied to demonstrable outcomes for those buyers with enough leverage to demand it.

The deeper question relates to what software vendors are actually selling. For many years they primarily sold access and the right to use a tool. What AI agents are forcing the industry to reckon with is a shift toward selling results, and that changes everything about how software companies build, price, support, and differentiate their products.