Fintech Sales Compensation Plans: How Companies are Balancing Growth and Risk

Fintech Sales Compensation Plans: How Companies are Balancing Growth and Risk

How you pay your sales team is a statement of principles. In fintech, where compliance failures cost millions and client churn decimates recurring revenue, it’s essential to devise a plan that encompasses all needs.

Fintech is not SaaS, which is a crucial distinction given the number of leaders who employ a standard software commission template, launch it company wide, and spend the next year tending to churned enterprise contracts, compliance violations, and a sales team optimized for bookings that never convert to healthy revenue.

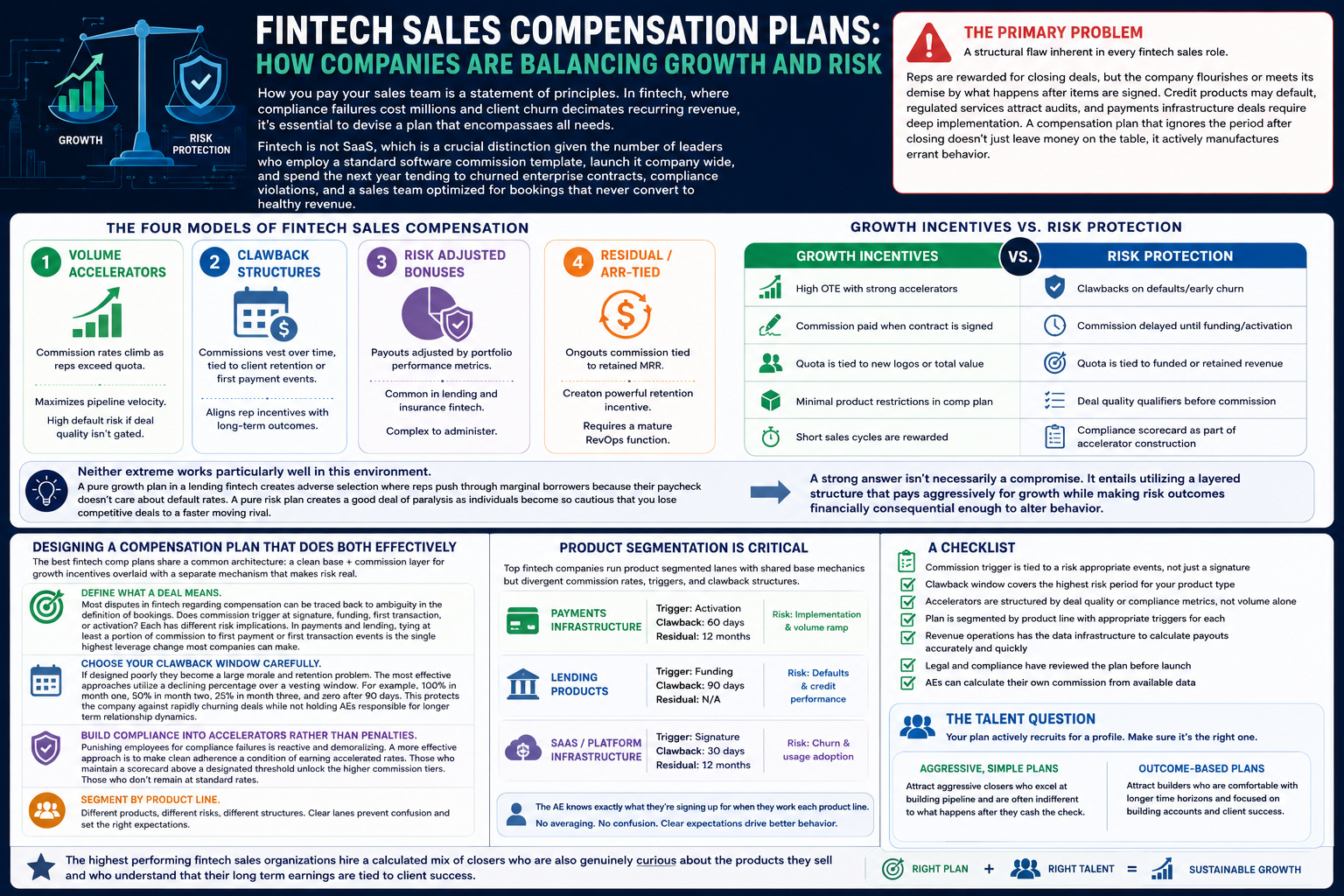

The primary problem is a structural flaw inherent in every fintech sales role. Reps are rewarded for closing deals, but the company flourishes or meets its demise by what happens after items are signed. Credit products may default, regulated services attract audits, and payments infrastructure deals require deep implementation. A compensation plan that ignores the period after closing doesn’t just leave money on the table, it actively manufactures errant behavior.

The four models of fintech sales compensation

Volume accelerators

Commission rates climb as reps exceed quota. Maximizes pipeline velocity. High default risk if deal quality isn’t gated

Clawback structures

Commissions vest over time, tied to client retention or first payment events. Aligns rep incentives with long-term outcomes

Risk adjusted bonuses

Payouts adjusted by portfolio performance metrics. Common in lending and insurance fintech. Complex to administer

Residual / ARR-tied

Ongoing commission tied to retained MRR. Creates powerful retention incentive. Requires a mature RevOps function

Every fintech compensation conversation eventually reaches the same focal point. Namely, how aggressively do you incentivize growth, and how much of that motivation do you tie to risk outcomes? The two forces tend to pull in opposite directions.

|

Growth Incentives |

Risk Protection |

|---|---|

|

High OTE with strong accelerators |

Clawbacks on defaults/early churn |

|

Commission paid when contract is signed |

Commission delayed until funding/activation |

|

Quota is tied to new logos or total value |

Quota is tied to funded or retained revenue |

|

Minimal product restrictions in comp plan |

Deal quality qualifiers before commission |

|

Short sales cycles are rewarded |

Compliance scorecard as part of accelerator construction |

Neither extreme works particularly well in this environment. A pure growth plan in a lending fintech creates adverse selection where reps push through marginal borrowers because their paycheck doesn’t care about default rates. A pure risk plan creates a good deal of paralysis as individuals become so cautious that you lose competitive deals to a faster moving rival.

A strong answer isn’t necessarily a compromise. It entails utilizing a layered structure that pays aggressively for growth while making risk outcomes financially consequential enough to alter behavior.

Designing a compensation plan that does both effectively

The best fintech comp plans we’ve encountered tend to share a common architecture that includes a clean base plus commission layer for growth incentives overlaid with a separate mechanism that makes risk real. Here’s a practical approach to building this type of structure:

• Define what a deal means. Most disputes in fintech regarding compensation can be traced back to ambiguity in the definition of bookings. Does commission trigger at signature, funding, first transaction, or activation? Each has different risk implications to take into consideration. In payments and lending, tying at least a portion of commission to first payment or first transaction events is the single highest leverage change most companies can make.

• Choose your clawback window carefully. These potentially carry emotional weight for fairly obvious reasons. If designed poorly they become a large morale and retention problem. The most effective approaches utilize a declining percentage over a vesting window. For example, 100% in month one, 50% in month two, 25% in month three, and zero after 90 days. This protects the company against rapidly churning deals while not holding account executives responsible for longer term relationship dynamics.

• Build compliance into accelerators rather than penalties. Punishing employees for compliance failures is reactive and demoralizing. A more effective approach that we’ve encountered is to make clean adherence a condition of earning accelerated rates. Those who maintain a scorecard above a designated threshold unlock the higher commission tiers. Those who don’t remain at standard rates.

One of the most common mistakes in fintech compensation design is running a single plan across highly disparate product types. An individual selling embedded payments infrastructure faces completely different risk profiles, sales cycle lengths, and post sale obligations than one working with consumer credit products. A unified plan forces an averaging that serves neither particularly well.

Top fintech companies run product segmented lanes with shared base mechanics but divergent commission rates, triggers, and clawback structures. Payments deals might pay at activation, lending deals pay at funding with a 90-day clawback, and SaaS infrastructure deals pay at signature with a 12-month residual. The AE knows exactly what they’re signing up for when they work each product line.

A checklist

• Commission trigger is tied to a risk appropriate events, not just a signature

• Clawback window covers the highest risk period for your product type

• Accelerators are structured by deal quality or compliance metrics rather than volume alone

• Plan is segmented by product line with appropriate triggers for each

• Revenue operations has the data infrastructure to calculate payouts accurately and quickly

• Legal and compliance have reviewed the plan before launch

• AE’s can calculate their own commission from available data

The talent question

There’s a secondary effect to designing systems for this realm that most fintech leaders underestimate. Namely, the type of sales talent your plan attracts and retains. Aggressive, simple commission structures garner the attention of aggressive closers who are excellent at building pipeline and often somewhat indifferent to what happens after they cash the check. Clawback heavy, outcome based plans tend to draw in people who are comfortable with longer time horizons and more interested in building accounts than initiating an all out dash to quota.

Neither profile is inherently correct, but your particular plan is actively recruiting for one of them. Make certain it’s targeting the profiles that match your product risk, your customer success capacity, and your regulatory environment. The highest performing fintech sales organizations we’ve observed tend to hire a calculated mix of closers who are also genuinely curious about the products they sell and who understand that their long term earnings are tied to client success.