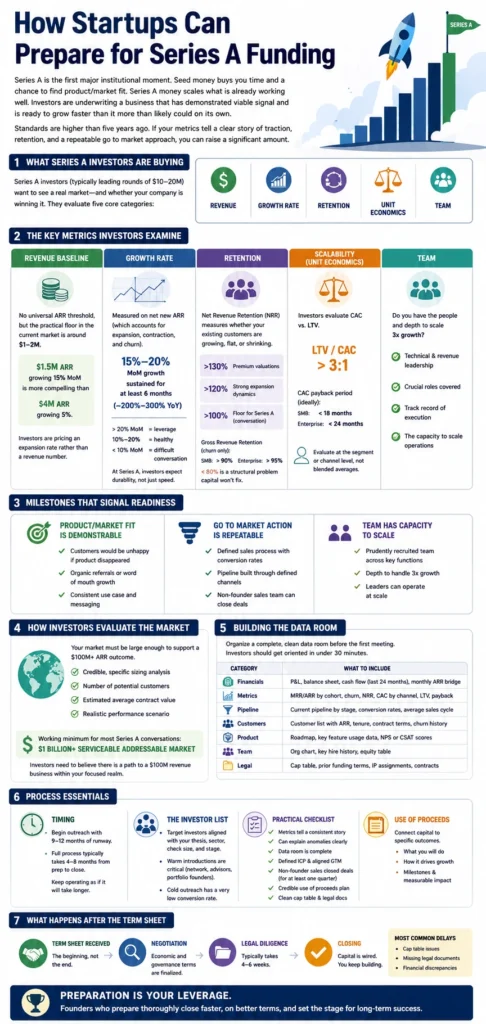

How Startups Can Prepare for Series A Funding

How Startups Can Prepare for Series A Funding

For most founders, Series A is the first major institutional moment.

Seed money buys you time and a chance to find a proper product/market fit while Series A money scales what is already working well. Investors at the Series A stage are underwriting a business that has demonstrated viable signal and is ready to grow faster than it more than likely could on its own.

The standards for this stage are now higher than they were five years ago as the market environment since then has pushed institutional investors toward fundamentals. If your metrics tell a clear story of traction, retention, and a repeatable go to market approach, you can raise a significant amount.

What Series A investors are buying

Series A investors, typically leading rounds between $10-20 million in the current environment, want to see that there a real market and, if so, is your company winning it? The metrics involved fall into a handful of categories including revenue, growth rate, retention, unit economics, and the team involved.

The revenue baseline

There is no universal annual recurring revenue threshold for a Series A, but the practical floor in the present market tends to be around $1 to 2M. A company at $1.5M ARR growing 15% month over month is a more compelling Series A candidate than one at $4M ARR growing 5%. Investors are pricing an expansion rate rather than a revenue number.

Growth rate

A month over month factor is typically the first metric an investor examines because it condenses a good deal of complexity into one primary signal. At the seed stage, investors will often forgive thin revenue if growth is strong. However, at Series A, the expectation is that you have enough data to show the expansion is durable.

The benchmark most investors that we work with maintain for a Series A ready SaaS company is 15% to 20% month over month growth sustained over at least six months, or roughly 200% to 300% year over year growth. Companies accelerating faster than that will have leverage in the process while those below 10% monthly will find the conversation more difficult. These numbers should be calculated on net new ARR, which accounts for expansion, contraction, and churn rather than simple client acquisition.

Retention

If there is one metric that separates fundable companies from those that need more time it’s net revenue retention. NRR measures whether your existing customer base is growing, flat, or shrinking over a given period of time. It effectively captures the combination of expansion revenue from upsells and the protraction from downgrades, cancellations, and other similar items.

The floor for a Series A conversation is NRR above 100%, meaning your existing customers are spending more over time than they were at the start of the measurement period. NRR above 120% signals a business with meaningful expansion dynamics, which is what allows a company to grow revenue without relying entirely on new customer acquisition. Businesses with NRR above 130% can make a compelling case for premium valuations.

Gross revenue retention, which measures only churn and does not account for expansion, should ideally be above 90% for SMB customers and above 95% for enterprise. Anything below 80% is a structural problem that capital will not immediately fix.

Scalability

Investors invariably want to see that the cost of acquiring a customer is justifiable relative to the revenue that customer generates. The two metrics that capture this are CAC (customer acquisition cost) and LTV (lifetime value).

The standard benchmark we hear on a fairly regular basis as one that will be productive is an LTV to CAC ratio above 3:1. That means for every dollar you spend acquiring a customer, you should expect to generate at least three dollars in lifetime gross profit. CAC payback period (how many months it takes to recover your acquisition cost) should ideally be under 18 months for SMB ventures and under 24 months for enterprise organizations.

These ratios tend to be most meaningful when calculated at the segment or channel level, not as blended averages across your entire business. A company with a 5:1 ratio from inbound organic and a 1.5:1 ratio from paid acquisition has a very different story than one with a clean 3:1 across the board.

Milestones that signal readiness

Metrics are necessary but not entirely sufficient as investors are also looking for evidence that the business has crossed a set of qualitative thresholds that indicate it is ready to scale. These marks do not show up neatly in a data page, but they shape how every number is interpreted.

Product/market fit is demonstrable, not theoretical. You should be able to point to a cohort of customers who would be unhappy if your product disappeared, evidence of organic referrals or word of mouth growth, and a use case that users describe in a consistent, similar manner. If your customers describe your product differently from each other, you have not yet found a concentrated mechanism.

Go to market action is repeatable. A Series A investor needs to believe that the money they put in will predictably generate more revenue. That requires a sales process with expected conversion rates, a pipeline that can be built through a defined set of channels, and some evidence that sales staff can close deals. If every sale depends on the CEO’s personal network, the model is not yet properly driven.

The team has the capacity to scale. Investors are assessing whether the founding organization has prudently recruited individuals who effectively cover crucial roles and has the depth to handle 3x growth. They are particularly focused on whether you have technical and revenue leadership that can operate at scale.

How investors evaluate the market

No matter how strong your metrics, a Series A investor will not write a check if the addressable market cannot support the growth trajectory implied by your round size. They are building funds with return targets that require some percentage of their portfolio companies to reach $100M in ARR or more. If your total addressable market cannot plausibly accommodate that outcome, the investment does not fit their model.

The practical implication is that your sizing analysis needs to be credible and specific. Investors have seen a plethora of inflated market slides. What they find compelling is an analysis that shows the number of potential customers, an estimated average contract value, and a realistic performance scenario.

For most Series A conversations, a serviceable addressable market of $1 billion or more is the working minimum. That does not mean the broader construct needs to be that large today. Rather, it implies that the investor needs to believe, based on your ICP definition and pricing, that there is a path to a $100M revenue business within your focused realm.

Building the data room

When you are ready to begin formal conversations with investors, the repository needs to be organized and complete before the first meeting, not assembled as diligence requests come in. Gaps will slow momentum and signal operational immaturity. These are some of the core components investors expect to find:

• Financials: P&L, balance sheet, cash flow statement (last 24 months), monthly ARR bridge

• Metrics: MRR/ARR by cohort, churn rates, NRR, CAC by channel, LTV, CAC payback

• Pipeline: Current pipeline by stage, conversion rates by stage, average sales cycle

• Customers: Full customer list with ARR, tenure, contract terms, churn history

• Product: Roadmap, key feature usage data, NPS or CSAT scores

• Team: Org chart, key hire history, equity table

• Legal: Cap table, prior funding terms, IP assignments, material contracts

Organize these items in a format that allows a sophisticated investor to get oriented in under 30 minutes. Use clear folder naming and avoid documents that require explanation to interpret. If your metrics require a glossary, rewrite the document.

Timing

Fundraising takes longer than many founders expect, and the timing of when you enter the market matters. The general guidance is to begin outreach when you have roughly nine to twelve months of runway remaining. Entering the process with less puts you in a negotiating position that is less than ideal.

The full process, from initial preparation through closing, typically takes four to eight months. Most rounds do not close in the compressed timelines founders envision thus build your schedule accordingly and continue operating as if the round will take longer than expected, because it usually does.

The investor list

Not every Series A investor is right for all companies. Targeting the right set of firms matters as much as the quality of your metrics. Investors have thesis areas, portfolio conflicts, check size preferences, and sector expertise that determine whether your company fits their model.

The most productive outreach comes from warm introductions through your existing investor network, advisors, and portfolio founders at firms you are targeting. Cold outreach to partners at major firms has a very low conversion rate. If you do not have the network to generate warm introductions, building that is a prerequisite to starting the fundraising process.

A practical checklist

Before entering a formal Series A process, work through the following:

• Your metrics tell a consistent story across ARR, growth rate, retention, and unit economics.

• You can explain any anomalies without hesitation.

• Your data room is complete and does not have gaps that would require weeks to fill.

• You have a defined ICP that you and your sales team describe in the same way.

• You have at least one quarter of data showing that non-founding sales staff can close deals.

• You have a credible use of proceeds narrative that connects the capital to specific outcomes.

• Your cap table is clean and your legal documents are current.

If any of these items require significant work, the right move is to delay the process until they are resolved. Entering the market before you are ready slows the capital raise, reduces your leverage, and signals to investors that the business is less mature than they need it to be.

What happens after the term sheet

Receiving this item is certainly not the end of the fundraising process as it’s just the beginning of a compressed negotiation on economic and governance terms, followed by legal diligence that can take four to six weeks. The most common delays in closing are cap table issues, missing legal documents, and financial discrepancies between what was presented and what diligence ultimately confirms.

The founders who close fastest are those who treated preparation as seriously as outreach. When those conditions are in place, the close is often a formality rather than a second fundraising process.