What Fintech Buyers Now Expect from Software Vendors

What Fintech Buyers Now Expect from Software Vendors

Fintech companies are now evaluating features and partners with equal diligence

The fintech landscape has matured dramatically over the past few years. After a decade of hypergrowth, a funding correction, and accelerating regulatory pressure, the buyers sitting across the table from software vendors today have amended their approach to vetting and utilizing products and services. They tend to be more skeptical, have a greater degree of operational sophistication, and are generally more demanding.

A software vendor that trying to win, retain, or expand within fintech accounts, must understand that this shift isn’t optional given recent events. Here’s what today’s fintech buyers now expect.

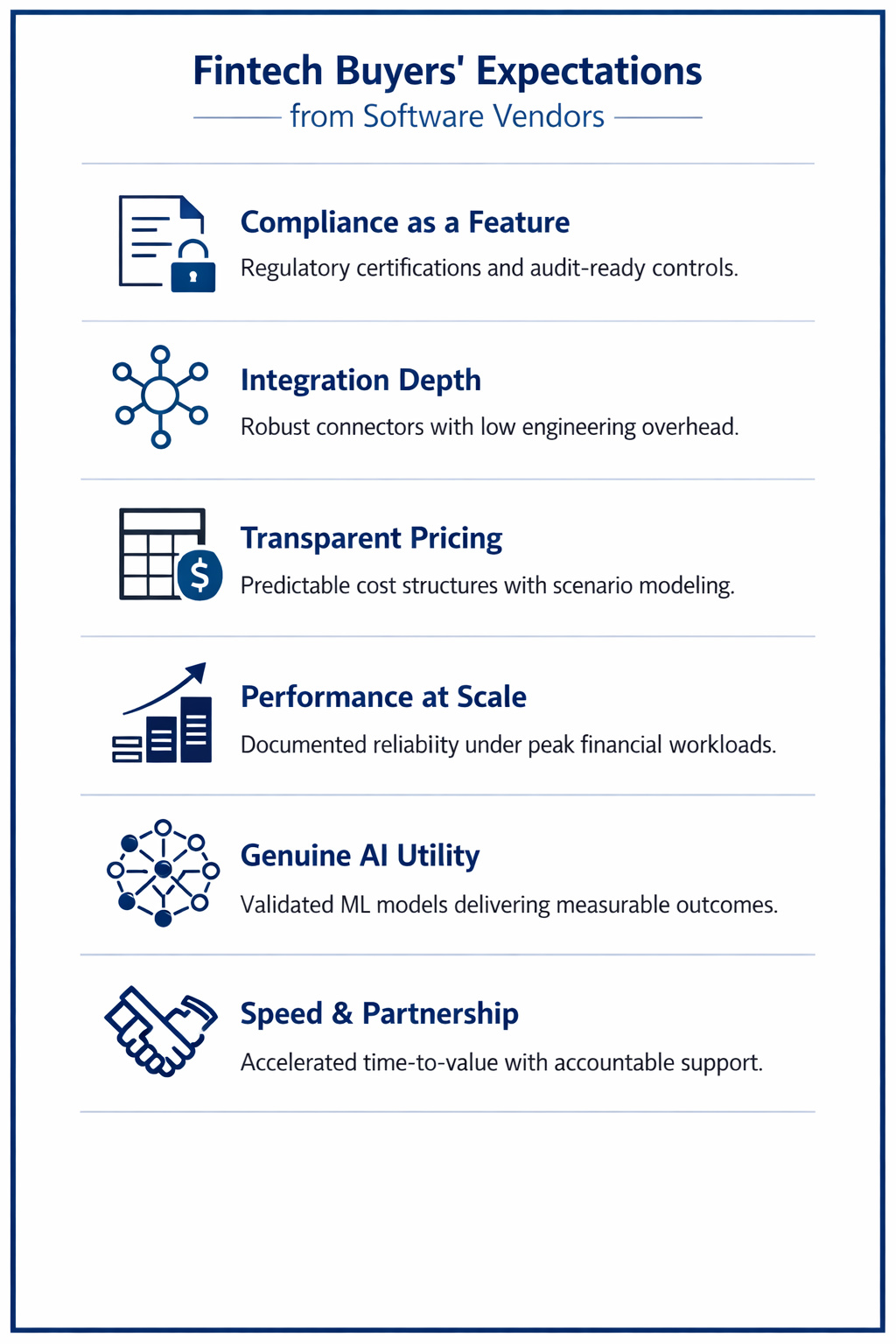

• Compliance is a feature

These companies operate in one of the most heavily scrutinized regulatory environments in technology. Whether it’s PCI-DSS, SOC 2 Type II, ISO 27001, GDPR, or the evolving landscape of regulations, compliance requirements are ubiquitous.

Given this, vendors now must recognize that compliance certifications, audit trails, data residency controls, and transparent security documentation are now baseline necessities. Those who are leading with these features tend to earn trust faster.

Buyers are also increasingly inquiring about future compliance readiness, particularly with regulators in the US, EU, and UK actively expanding fintech oversight.

• Integration Depth

The average fintech company employs dozens of tools including payment processors, core banking systems, fraud engines, data warehouses, CRMs, and more. They have deemed these items fairly essential to know:

• How many engineering hours does the initial integration actually take?

• What’s the ongoing maintenance demand when either side updates?

• Is there native support for the specific platforms they use?

Vendors who invest in pre-built, well documented connectors and maintain them proactively win more deals. Those who hand buyers a generic REST API and call it good are losing to competitors who’ve completed the now necessary framework.

• Transparent, Predictable Pricing

Usage based pricing is rapidly gaining in popularity popular, but unpredictability is loathed by fintech finance teams working within tight budgets. After years of surprise invoices tied to transaction volumes, API calls, or seat expansions, fintech buyers have become acutely sensitive to pricing models that obscure total cost of ownership.

They are now seeking honest, scenario outlined pricing conversations upfront, and want to model what they’ll pay at given rates in a particular economic environment. Vendors who utilize this transparency build more durable relationships than those who simply optimize for the initial deal.

Enterprise pricing tiers that include genuine value (dedicated support, SLAs with proper backing, and detailed compliance documentation) are being far better received than inflated list prices with arbitrary discounts.

• Proven Performance at Scale

A slate of recognizable financial services logos certainly still helps to close deals. However, it’s now also essential to be able to answer these questions:

• What transaction volumes has this vendor actually processed in production?

• How did the system perform during peak periods including tax season, market volatility, and times of high scale payments?

• What’s the documented uptime over the past 12 months and what happened during unforeseen incidents?

Reference calls appear to have gained even more importance in the process and buyers are approaching them with specific, technical questions. Vendors who proactively offer detailed case studies and honest performance benchmarks stand out.

• Genuine AI Utility

Every software vendor now claims have AI as a base component in 2026. Fintech buyers have developed a keen sense for the difference between genuine machine learning embedded in core workflows and something bolted onto an existing product. Knowing that there is still a strong human element involved is required.

Fraud detection, document processing, credit underwriting support, and anomaly detection in transactions are areas where AI is faring well, but be prepared to show it working on real data.

• Speed to Actual Value

Fintech companies (particularly growth stage ventures) have become far more disciplined about the time it take to realize value since the funding environment contracted. Long implementation timelines, complex onboarding processes, and extended professional services engagements are now often deal breakers where they used to be somewhat accepted norms. Customer success teams are becoming ever more essential.

• A true partnership

Perhaps the most significant change is more philosophical. Fintech companies that have been burned by vendors who disappeared after contract signature are explicitly looking for evidence of partnership before they sign and agreement.

They want to see a named customer success manager with relevant fintech experience, executive sponsorship for strategic accounts, a product roadmap they can influence, and a support model that reflects the urgency of financial services operations.

The vendors thriving in fintech aren’t just selling software. They’re embedding themselves in their customers’ growth by sharing knowledge, rapidly identifying risks, and participating as stakeholders in their success.